Portfolio Optimization with Multivariate GARCH Model Comparison

Martin Hoshi Vognsen

10:06 31 January 2026

portfolio-optimization-demo.Rmd

## =============================================================================

## GLOBAL SETTINGS - Adjust these to control computation time and data source

## =============================================================================

## Set to TRUE for full analysis, FALSE for quick demo

FULL_ANALYSIS <- FALSE

## Data source: "package" uses pre-downloaded data from tsbs package

## "download" fetches fresh data from Yahoo Finance

DATA_SOURCE <- "package" ## Options: "package" or "download"

if (FULL_ANALYSIS) {

max_num_rb <- 10 ## Number of rebalances with bootstrap

max_iter <- 20 ## Maximum EM iterations per model

num_boots <- 100 ## Bootstrap replicates per rebalance

train_window <- 504 ## ~2 years training

} else {

max_num_rb <- 3 ## Quick demo: 3 rebalances

max_iter <- 3 ## Quick demo: 3 iterations

num_boots <- 30 ## Quick demo: 30 replicates

train_window <- 252 ## Quick demo: 1 year training

}

collect_diagnostics <- TRUE

verbose <- FALSE

return_fit <- TRUEIntroduction

This vignette demonstrates advanced portfolio optimization using the tsbs package’s Markov-Switching VARMA-GARCH bootstrap framework. We compare three multivariate GARCH correlation structures:

- DCC (Dynamic Conditional Correlation): The workhorse model with explicit correlation dynamics

- CGARCH (Copula GARCH): Separates marginals from dependence via copula theory

- GOGARCH (Generalized Orthogonal GARCH): Uses ICA to extract independent factors

Each model captures time-varying correlations differently, leading to potentially different portfolio allocations and uncertainty quantification.

Key Features Demonstrated

- Six portfolio optimization strategies with real market data

- Out-of-sample backtesting with quarterly rebalancing

- Bootstrap uncertainty quantification comparing all three GARCH models

-

Bootstrap diagnostics using the

tsbs_diagnosticssystem - Comprehensive performance analysis with transaction costs

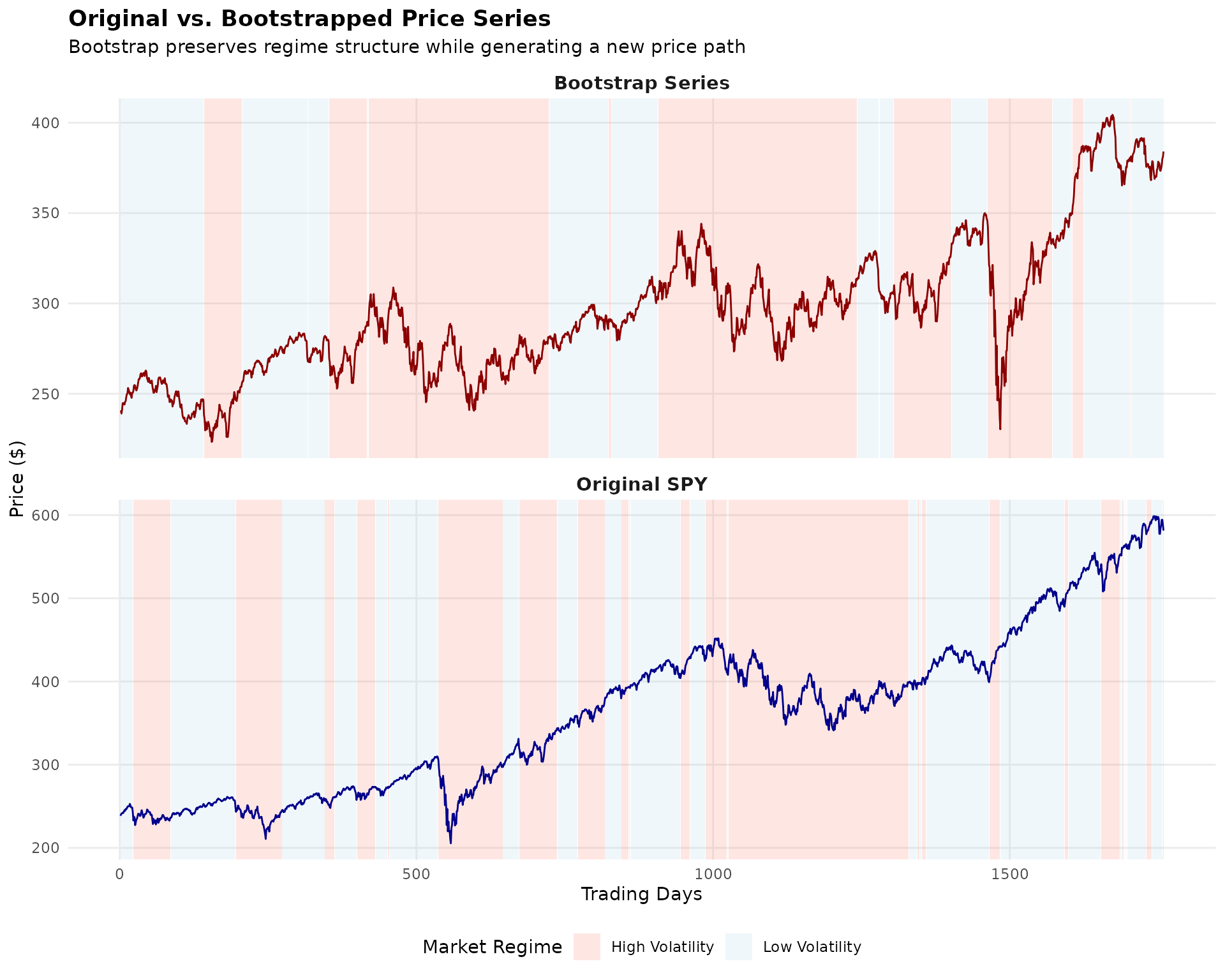

What is a Bootstrapped Series?

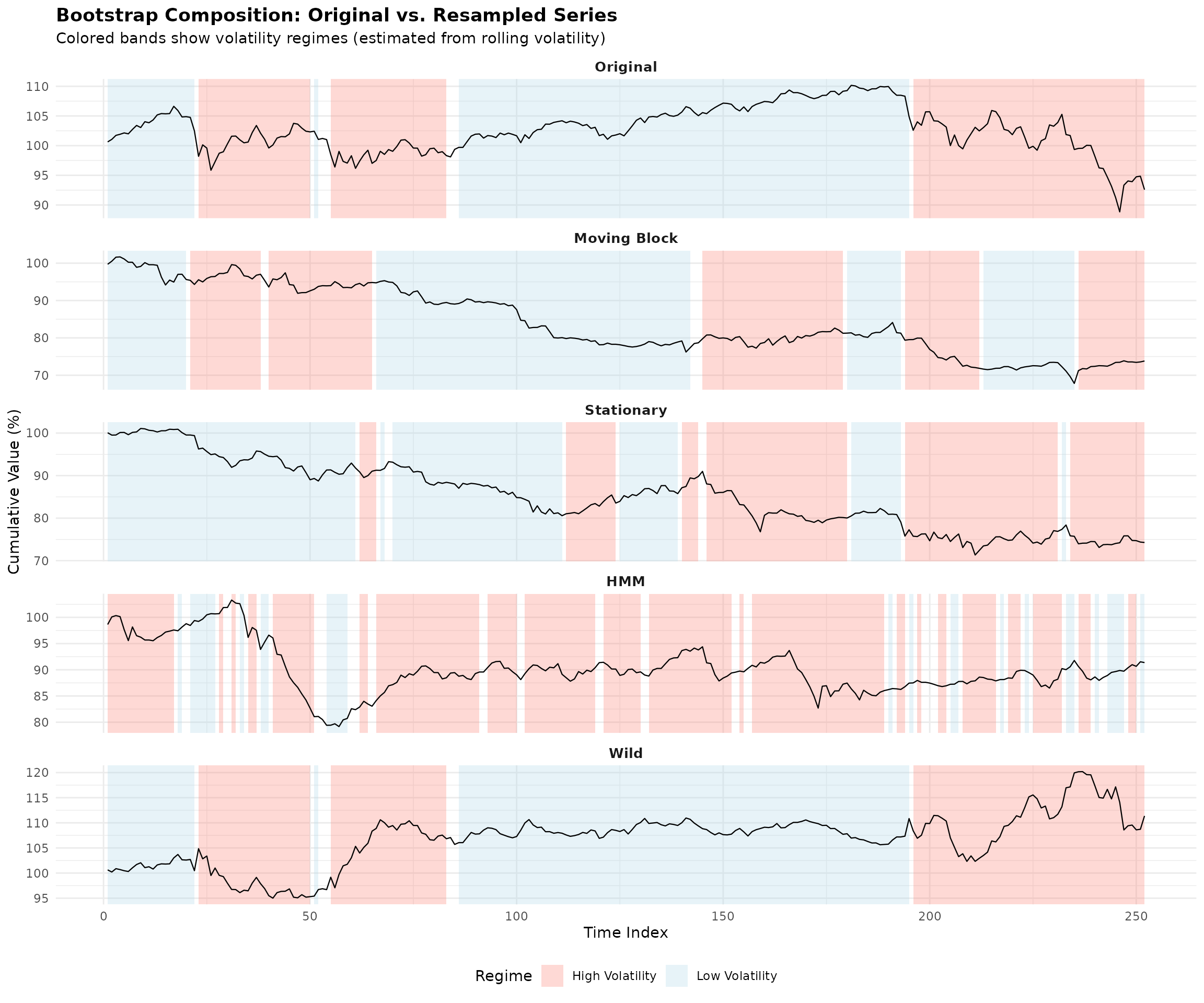

Before diving into portfolio optimization, let’s visualize what the MS-VARMA-GARCH bootstrap actually produces. The basic idea is:

- Take raw price data and compute log-returns

- Fit a Markov-Switching model that identifies different market regimes (e.g., calm vs. volatile periods)

- Generate new return series by resampling blocks of returns while respecting the regime structure

- Convert the bootstrapped returns back to a synthetic price series

The plot below shows an original SPY price series alongside a bootstrapped version. The colored bands indicate the estimated market regimes—notice how the bootstrap preserves the general character of each regime while creating a genuinely new path.

The bootstrap series (bottom panel) is not a forecast—it’s a plausible alternative history that could have occurred given the same underlying market dynamics. By generating many such series and computing portfolio weights on each, we can quantify how uncertain our optimal allocation really is.

Part 1: Portfolio Optimization Functions

## =============================================================================

## PORTFOLIO OPTIMIZATION FUNCTIONS

## =============================================================================

## 1.1 Minimum Variance Portfolio

min_variance_portfolio <- function(returns, ...) {

Sigma <- cov(returns)

n <- ncol(returns)

if (requireNamespace("quadprog", quietly = TRUE)) {

Dmat <- 2 * Sigma + diag(1e-8, n)

dvec <- rep(0, n)

Amat <- cbind(rep(1, n), diag(n))

bvec <- c(1, rep(0, n))

sol <- tryCatch(

quadprog::solve.QP(Dmat, dvec, Amat, bvec, meq = 1),

error = function(e) NULL

)

if (!is.null(sol)) {

weights <- pmax(sol$solution, 0)

weights <- weights / sum(weights)

} else {

weights <- rep(1/n, n)

}

} else {

ones <- rep(1, n)

Sigma_inv <- tryCatch(solve(Sigma + diag(1e-6, n)),

error = function(e) diag(1/diag(Sigma)))

weights <- as.vector(Sigma_inv %*% ones) / as.vector(t(ones) %*% Sigma_inv %*% ones)

weights <- pmax(weights, 0)

weights <- weights / sum(weights)

}

names(weights) <- colnames(returns)

weights

}

## 1.2 Maximum Sharpe Ratio Portfolio

max_sharpe_portfolio <- function(returns, rf = 0, ...) {

mu <- colMeans(returns)

Sigma <- cov(returns)

n <- ncol(returns)

mu_excess <- mu - rf

if (all(mu_excess <= 0)) {

return(min_variance_portfolio(returns))

}

if (requireNamespace("quadprog", quietly = TRUE)) {

Dmat <- 2 * Sigma + diag(1e-8, n)

dvec <- rep(0, n)

Amat <- cbind(mu_excess, diag(n))

bvec <- c(1, rep(0, n))

sol <- tryCatch(

quadprog::solve.QP(Dmat, dvec, Amat, bvec, meq = 1),

error = function(e) NULL

)

if (!is.null(sol) && sum(sol$solution) > 0) {

weights <- pmax(sol$solution, 0)

weights <- weights / sum(weights)

} else {

weights <- min_variance_portfolio(returns)

}

} else {

weights <- min_variance_portfolio(returns)

}

names(weights) <- colnames(returns)

weights

}

## 1.3 Risk Parity Portfolio

risk_parity_portfolio <- function(returns, ...) {

Sigma <- cov(returns)

n <- ncol(returns)

vols <- sqrt(diag(Sigma))

if (any(!is.finite(vols)) || any(vols < 1e-10)) {

weights <- rep(1/n, n)

names(weights) <- colnames(returns)

return(weights)

}

weights <- 1 / vols

weights <- weights / sum(weights)

for (iter in 1:20) {

port_vol <- sqrt(t(weights) %*% Sigma %*% weights)

if (!is.finite(port_vol) || port_vol < 1e-10) break

mrc <- (Sigma %*% weights) / as.numeric(port_vol)

rc <- weights * mrc

target_rc <- sum(rc) / n

adjustment <- target_rc / (rc + 1e-8)

weights <- weights * sqrt(pmax(adjustment, 0))

if (sum(weights) < 1e-10 || any(!is.finite(weights))) {

weights <- rep(1/n, n)

break

}

weights <- weights / sum(weights)

}

names(weights) <- colnames(returns)

weights

}

## 1.4 Black-Litterman Portfolio

black_litterman_portfolio <- function(returns, risk_aversion = 2.5, tau = 0.05, ...) {

mu_hist <- colMeans(returns)

Sigma <- cov(returns)

n <- ncol(returns)

w_mkt <- rep(1/n, n)

pi <- risk_aversion * Sigma %*% w_mkt

P <- diag(n)

Q <- mu_hist

omega_diag <- diag(Sigma) * tau

Omega <- diag(omega_diag)

tau_Sigma <- tau * Sigma

tau_Sigma_inv <- solve(tau_Sigma + diag(1e-8, n))

Omega_inv <- solve(Omega + diag(1e-8, n))

M_inv <- tau_Sigma_inv + t(P) %*% Omega_inv %*% P

M <- solve(M_inv + diag(1e-8, n))

mu_bl <- M %*% (tau_Sigma_inv %*% pi + t(P) %*% Omega_inv %*% Q)

if (requireNamespace("quadprog", quietly = TRUE)) {

Sigma_bl <- Sigma + tau_Sigma

Dmat <- 2 * risk_aversion * Sigma_bl + diag(1e-8, n)

dvec <- as.vector(mu_bl)

Amat <- cbind(rep(1, n), diag(n))

bvec <- c(1, rep(0, n))

sol <- tryCatch(

quadprog::solve.QP(Dmat, dvec, Amat, bvec, meq = 1),

error = function(e) NULL

)

if (!is.null(sol)) {

weights <- pmax(sol$solution, 0)

weights <- weights / sum(weights)

} else {

weights <- rep(1/n, n)

}

} else {

weights <- rep(1/n, n)

}

names(weights) <- colnames(returns)

weights

}

## 1.5 Mean-Variance with Shrinkage (Ledoit-Wolf)

shrinkage_portfolio <- function(returns, target_return = NULL, ...) {

mu <- colMeans(returns)

n <- ncol(returns)

T_obs <- nrow(returns)

S <- cov(returns)

trace_S <- sum(diag(S))

F_target <- (trace_S / n) * diag(n)

X <- scale(returns, center = TRUE, scale = FALSE)

sum_sq <- sum(S^2)

delta <- min(1, max(0, (1/T_obs) / (sum_sq / n + 1e-8)))

Sigma_shrunk <- delta * F_target + (1 - delta) * S

if (requireNamespace("quadprog", quietly = TRUE)) {

Dmat <- 2 * Sigma_shrunk + diag(1e-8, n)

dvec <- rep(0, n)

Amat <- cbind(rep(1, n), diag(n))

bvec <- c(1, rep(0, n))

sol <- tryCatch(

quadprog::solve.QP(Dmat, dvec, Amat, bvec, meq = 1),

error = function(e) NULL

)

if (!is.null(sol)) {

weights <- pmax(sol$solution, 0)

weights <- weights / sum(weights)

} else {

weights <- rep(1/n, n)

}

} else {

weights <- rep(1/n, n)

}

names(weights) <- colnames(returns)

weights

}

## 1.6 Equal Weight (Benchmark)

equal_weight_portfolio <- function(returns, ...) {

n <- ncol(returns)

weights <- rep(1/n, n)

names(weights) <- colnames(returns)

weights

}

## Portfolio performance metrics

calc_portfolio_metrics <- function(returns, weights) {

port_ret <- as.vector(returns %*% weights)

ann_factor <- 252

mean_ret <- mean(port_ret) * ann_factor

vol <- sd(port_ret) * sqrt(ann_factor)

sharpe <- mean_ret / vol

cum_ret <- cumprod(1 + port_ret)

rolling_max <- cummax(cum_ret)

drawdown <- (cum_ret - rolling_max) / rolling_max

max_dd <- min(drawdown)

downside_ret <- port_ret[port_ret < 0]

downside_dev <- if (length(downside_ret) > 1) sd(downside_ret) * sqrt(ann_factor) else vol

sortino <- mean_ret / downside_dev

c(

"Ann.Return" = mean_ret * 100,

"Ann.Vol" = vol * 100,

"Sharpe" = sharpe,

"Sortino" = sortino,

"MaxDD" = max_dd * 100

)

}Part 2: Data Download and Preparation

## =======================================================================## ADVANCED PORTFOLIO OPTIMIZATION WITH MULTIVARIATE GARCH COMPARISON## =======================================================================

## Asset information

symbols <- c("SPY", "EFA", "BND", "GLD", "VNQ")

symbol_names <- c("US Equity", "Intl Equity", "US Bonds", "Gold", "REITs")

if (DATA_SOURCE == "package") {

## -------------------------------------------------------------------------

## Option 1: Use pre-downloaded data from tsbs package

## -------------------------------------------------------------------------

data("etf_returns", package = "tsbs")

y_full <- etf_returns

dates_full <- attr(etf_returns, "dates")

symbols <- attr(etf_returns, "symbols")

symbol_names <- attr(etf_returns, "symbol_names")

cat("\nUsing package data (etf_returns)\n")

cat(" Source:", attr(etf_returns, "source"), "\n")

cat(" Downloaded:", as.character(attr(etf_returns, "download_date")), "\n")

} else {

## -------------------------------------------------------------------------

## Option 2: Download fresh data from Yahoo Finance

## -------------------------------------------------------------------------

start_date <- "2018-01-01"

end_date <- Sys.Date()

cat("\nDownloading fresh data from Yahoo Finance...\n")

cat(" Symbols:", paste(symbols, collapse = ", "), "\n")

cat(" Date range:", start_date, "to", as.character(end_date), "\n")

prices_list <- lapply(symbols, function(sym) {

tryCatch({

getSymbols(sym, src = "yahoo", from = start_date, to = end_date,

auto.assign = FALSE)

}, error = function(e) {

warning(paste("Failed to download", sym))

NULL

})

})

valid_idx <- !sapply(prices_list, is.null)

if (sum(valid_idx) < 3) {

stop("Could not download enough symbols. Check internet connection.")

}

symbols <- symbols[valid_idx]

symbol_names <- symbol_names[valid_idx]

prices_list <- prices_list[valid_idx]

adj_close <- do.call(merge, lapply(prices_list, Ad))

colnames(adj_close) <- symbols

adj_close <- na.omit(adj_close)

returns_xts <- diff(log(adj_close)) * 100

returns_xts <- na.omit(returns_xts)

y_full <- as.matrix(coredata(returns_xts))

dates_full <- index(returns_xts)

}##

## Using package data (etf_returns)

## Source: Yahoo Finance via quantmod

## Downloaded: 2026-01-21

k <- ncol(y_full)##

## Data summary:## Period: 2018-01-03 to 2024-12-30## Observations: 1759## Assets: SPY, EFA, BND, GLD, VNQ## -----------------------------------------------------------------------## IN-SAMPLE STATISTICS## -----------------------------------------------------------------------##

## Annualized statistics:

ann_stats <- rbind(

"Return (%)" = colMeans(y_full) * 252,

"Vol (%)" = apply(y_full, 2, sd) * sqrt(252),

"Sharpe" = colMeans(y_full) / apply(y_full, 2, sd) * sqrt(252)

)

print(round(ann_stats, 2))## SPY EFA BND GLD VNQ

## Return (%) 12.84 3.90 1.06 9.37 4.79

## Vol (%) 19.54 18.27 6.16 14.33 23.12

## Sharpe 0.66 0.21 0.17 0.65 0.21##

## Correlation matrix:## SPY EFA BND GLD VNQ

## SPY 1.00 0.87 0.16 0.11 0.76

## EFA 0.87 1.00 0.20 0.21 0.71

## BND 0.16 0.20 1.00 0.36 0.29

## GLD 0.11 0.21 0.36 1.00 0.16

## VNQ 0.76 0.71 0.29 0.16 1.00Part 3: Model Specifications

We define specifications for three multivariate GARCH model types:

-

DCC: Uses

dcc_modelspecwith correlation dynamics (α, β) -

CGARCH: Uses

cgarch_modelspecwith copula-based dependence -

GOGARCH: Uses

gogarch_modelspecwith ICA decomposition

## =============================================================================

## MODEL SPECIFICATIONS FOR DCC, CGARCH, AND GOGARCH

## =============================================================================

## --- DCC Specification ---

make_dcc_spec <- function(omega, alpha, beta, dcc_alpha, dcc_beta, k) {

list(

var_order = 1,

garch_spec_fun = "dcc_modelspec",

distribution = "mvn",

garch_spec_args = list(

dcc_order = c(1, 1),

dynamics = "dcc",

garch_model = list(

univariate = lapply(1:k, function(i) {

list(model = "garch", garch_order = c(1, 1), distribution = "norm")

})

)

),

start_pars = list(

var_pars = rep(0, k * (1 + k)),

garch_pars = lapply(1:k, function(i) {

list(omega = omega[i], alpha1 = alpha[i], beta1 = beta[i])

}),

dcc_pars = list(alpha_1 = dcc_alpha, beta_1 = dcc_beta),

dist_pars = NULL

)

)

}

spec_dcc <- list(

make_dcc_spec(

omega = rep(0.02, k), alpha = rep(0.05, k), beta = rep(0.90, k),

dcc_alpha = 0.02, dcc_beta = 0.95, k = k

),

make_dcc_spec(

omega = rep(0.08, k), alpha = rep(0.12, k), beta = rep(0.80, k),

dcc_alpha = 0.06, dcc_beta = 0.90, k = k

)

)

## --- CGARCH Specification ---

make_cgarch_spec <- function(omega, alpha, beta, dcc_alpha, dcc_beta, k,

copula = "mvn", transformation = "parametric") {

list(

var_order = 1,

garch_spec_fun = "cgarch_modelspec",

distribution = copula,

garch_spec_args = list(

dcc_order = c(1, 1),

dynamics = "dcc",

transformation = transformation,

copula = copula,

garch_model = list(

univariate = lapply(1:k, function(i) {

list(model = "garch", garch_order = c(1, 1), distribution = "norm")

})

)

),

start_pars = list(

var_pars = rep(0, k * (1 + k)),

garch_pars = lapply(1:k, function(i) {

list(omega = omega[i], alpha1 = alpha[i], beta1 = beta[i])

}),

dcc_pars = list(alpha_1 = dcc_alpha, beta_1 = dcc_beta),

dist_pars = list(shape = 6) ## For MVT copula

)

)

}

# spec_cgarch <- list(

# make_cgarch_spec(

# omega = rep(0.02, k), alpha = rep(0.05, k), beta = rep(0.90, k),

# dcc_alpha = 0.02, dcc_beta = 0.95, k = k,

# copula = "mvn", transformation = "parametric"

# ),

# make_cgarch_spec(

# omega = rep(0.08, k), alpha = rep(0.12, k), beta = rep(0.80, k),

# dcc_alpha = 0.06, dcc_beta = 0.90, k = k,

# copula = "mvn", transformation = "parametric"

# )

# )

spec_cgarch <- list(

make_cgarch_spec(

omega = rep(0.02, k), alpha = rep(0.05, k), beta = rep(0.90, k),

dcc_alpha = 0.02, dcc_beta = 0.95, k = k,

copula = "mvt", transformation = "parametric"

),

make_cgarch_spec(

omega = rep(0.08, k), alpha = rep(0.12, k), beta = rep(0.80, k),

dcc_alpha = 0.06, dcc_beta = 0.90, k = k,

copula = "mvt", transformation = "parametric"

)

)

## --- GOGARCH Specification ---

make_gogarch_spec <- function(omega, alpha, beta, k) {

list(

var_order = 1,

garch_spec_fun = "gogarch_modelspec",

distribution = "norm",

garch_spec_args = list(

model = "garch",

order = c(1, 1),

ica = "radical",

components = k

),

start_pars = list(

var_pars = rep(0, k * (1 + k)),

garch_pars = lapply(1:k, function(i) {

list(omega = omega[i], alpha1 = alpha[i], beta1 = beta[i])

}),

dist_pars = NULL

)

)

}

spec_gogarch <- list(

make_gogarch_spec(

omega = rep(0.02, k), alpha = rep(0.05, k), beta = rep(0.90, k), k = k

),

make_gogarch_spec(

omega = rep(0.08, k), alpha = rep(0.12, k), beta = rep(0.80, k), k = k

)

)##

## Model specifications created:## - DCC: 2 regime states with DCC(1,1) dynamics## - CGARCH: 2 regime states with MVN copula## - GOGARCH: 2 regime states with RADICAL ICAPart 4: Backtest Setup

## =======================================================================## OUT-OF-SAMPLE BACKTEST## =======================================================================

## Parameters

rebalance_freq <- 63 ## Quarterly rebalancing

n_total <- nrow(y_full)

rebalance_dates <- seq(train_window + 1, n_total - rebalance_freq, by = rebalance_freq)##

## Backtest setup:## Training window: 252 days## Rebalance frequency: 63 days (~quarterly)## Number of rebalances: 23## Bootstrap replicates per rebalance: 30## Max rebalances with bootstrap: 3

## Strategies to test

strategies <- list(

"Equal Weight" = equal_weight_portfolio,

"Min Variance" = min_variance_portfolio,

"Max Sharpe" = max_sharpe_portfolio,

"Risk Parity" = risk_parity_portfolio,

"Black-Litterman" = black_litterman_portfolio,

"Shrinkage" = shrinkage_portfolio

)

## Storage for results

backtest_returns <- matrix(NA, nrow = n_total - train_window, ncol = length(strategies))

colnames(backtest_returns) <- names(strategies)

weight_history <- lapply(strategies, function(x) {

matrix(NA, nrow = length(rebalance_dates), ncol = k)

})Part 5: Multi-Model Bootstrap Backtest

This is the core of our analysis. For each rebalance period, we run bootstrap using all three GARCH model types and compare their uncertainty estimates.

## =============================================================================

## RUN BACKTEST WITH DCC, CGARCH, AND GOGARCH COMPARISON

## =============================================================================

cat("\nRunning backtest with multi-model bootstrap comparison...\n")

set.seed(42)

current_weights <- lapply(strategies, function(x) rep(1/k, k))

pb <- txtProgressBar(min = 0, max = length(rebalance_dates), style = 3)

## Storage for bootstrap results from each model type

boot_results_dcc <- list()

boot_results_cgarch <- list()

boot_results_gogarch <- list()

## Storage for diagnostics from each model

diagnostics_dcc <- list()

diagnostics_cgarch <- list()

diagnostics_gogarch <- list()

for (rb_idx in seq_along(rebalance_dates)) {

rb_date <- rebalance_dates[rb_idx]

## Training data

train_start <- rb_date - train_window

train_end <- rb_date - 1

y_train <- y_full[train_start:train_end, ]

## Compute new weights for each strategy

for (strat_name in names(strategies)) {

strat_func <- strategies[[strat_name]]

tryCatch({

new_weights <- strat_func(y_train)

current_weights[[strat_name]] <- new_weights

weight_history[[strat_name]][rb_idx, ] <- new_weights

}, error = function(e) {

## Keep previous weights on error

})

}

## Run multi-model bootstrap for first max_num_rb rebalances

if (rb_idx <= max_num_rb) {

## --- DCC Bootstrap ---

result_dcc <- tryCatch({

boot_result <- tsbs(

x = y_train,

bs_type = "ms_varma_garch",

num_boots = num_boots,

num_blocks = 15,

num_states = 2,

spec = spec_dcc,

model_type = "multivariate",

func = risk_parity_portfolio,

apply_func_to = "all",

control = list(max_iter = max_iter, tol = 1e-2),

parallel = TRUE,

num_cores = 4,

return_fit = return_fit,

collect_diagnostics = collect_diagnostics

)

list(

weights = do.call(rbind, lapply(boot_result$func_outs, function(w) t(w))),

diagnostics = if(collect_diagnostics && return_fit) boot_result$fit$diagnostics else NULL

)

}, error = function(e) {

message("DCC bootstrap failed at rebalance ", rb_idx, ": ", e$message)

NULL

})

if (!is.null(result_dcc)) {

boot_results_dcc[[rb_idx]] <- result_dcc$weights

diagnostics_dcc[[rb_idx]] <- result_dcc$diagnostics

}

## --- CGARCH Bootstrap ---

result_cgarch <- tryCatch({

boot_result <- tsbs(

x = y_train,

bs_type = "ms_varma_garch",

num_boots = num_boots,

num_blocks = 15,

num_states = 2,

spec = spec_cgarch,

model_type = "multivariate",

func = risk_parity_portfolio,

apply_func_to = "all",

control = list(max_iter = max_iter, tol = 1e-2),

parallel = TRUE,

num_cores = 4,

return_fit = return_fit,

collect_diagnostics = collect_diagnostics

)

list(

weights = do.call(rbind, lapply(boot_result$func_outs, function(w) t(w))),

diagnostics = if(collect_diagnostics && return_fit) boot_result$fit$diagnostics else NULL

)

}, error = function(e) {

message("CGARCH bootstrap failed at rebalance ", rb_idx, ": ", e$message)

NULL

})

if (!is.null(result_cgarch)) {

boot_results_cgarch[[rb_idx]] <- result_cgarch$weights

diagnostics_cgarch[[rb_idx]] <- result_cgarch$diagnostics

}

## --- GOGARCH Bootstrap ---

result_gogarch <- tryCatch({

boot_result <- tsbs(

x = y_train,

bs_type = "ms_varma_garch",

num_boots = num_boots,

num_blocks = 15,

num_states = 2,

spec = spec_gogarch,

model_type = "multivariate",

func = risk_parity_portfolio,

apply_func_to = "all",

control = list(max_iter = max_iter, tol = 1e-2),

parallel = TRUE,

num_cores = 4,

return_fit = return_fit,

collect_diagnostics = collect_diagnostics

)

list(

weights = do.call(rbind, lapply(boot_result$func_outs, function(w) t(w))),

diagnostics = if(collect_diagnostics && return_fit) boot_result$fit$diagnostics else NULL

)

}, error = function(e) {

message("GOGARCH bootstrap failed at rebalance ", rb_idx, ": ", e$message)

NULL

})

if (!is.null(result_gogarch)) {

boot_results_gogarch[[rb_idx]] <- result_gogarch$weights

diagnostics_gogarch[[rb_idx]] <- result_gogarch$diagnostics

}

}

## Calculate returns until next rebalance

if (rb_idx < length(rebalance_dates)) {

next_rb <- rebalance_dates[rb_idx + 1]

} else {

next_rb <- n_total

}

hold_period <- rb_date:(next_rb - 1)

hold_returns <- y_full[hold_period, , drop = FALSE]

for (strat_name in names(strategies)) {

w <- current_weights[[strat_name]]

port_ret <- hold_returns %*% w

result_idx <- hold_period - train_window

backtest_returns[result_idx, strat_name] <- port_ret

}

setTxtProgressBar(pb, rb_idx)

}

close(pb)

cat("\nBacktest completed!\n")Part 6: Backtest Results

## -----------------------------------------------------------------------## BACKTEST RESULTS## -----------------------------------------------------------------------

## Remove NA rows

backtest_returns <- backtest_returns[complete.cases(backtest_returns), ]

## Calculate performance metrics

perf_summary <- t(sapply(colnames(backtest_returns), function(strat) {

ret <- backtest_returns[, strat]

ann_ret <- mean(ret) * 252

ann_vol <- sd(ret) * sqrt(252)

sharpe <- ann_ret / ann_vol

cum_ret <- cumprod(1 + ret/100)

rolling_max <- cummax(cum_ret)

max_dd <- min((cum_ret - rolling_max) / rolling_max)

c(

"Ann.Return(%)" = ann_ret,

"Ann.Vol(%)" = ann_vol,

"Sharpe" = sharpe,

"MaxDD(%)" = max_dd * 100

)

}))##

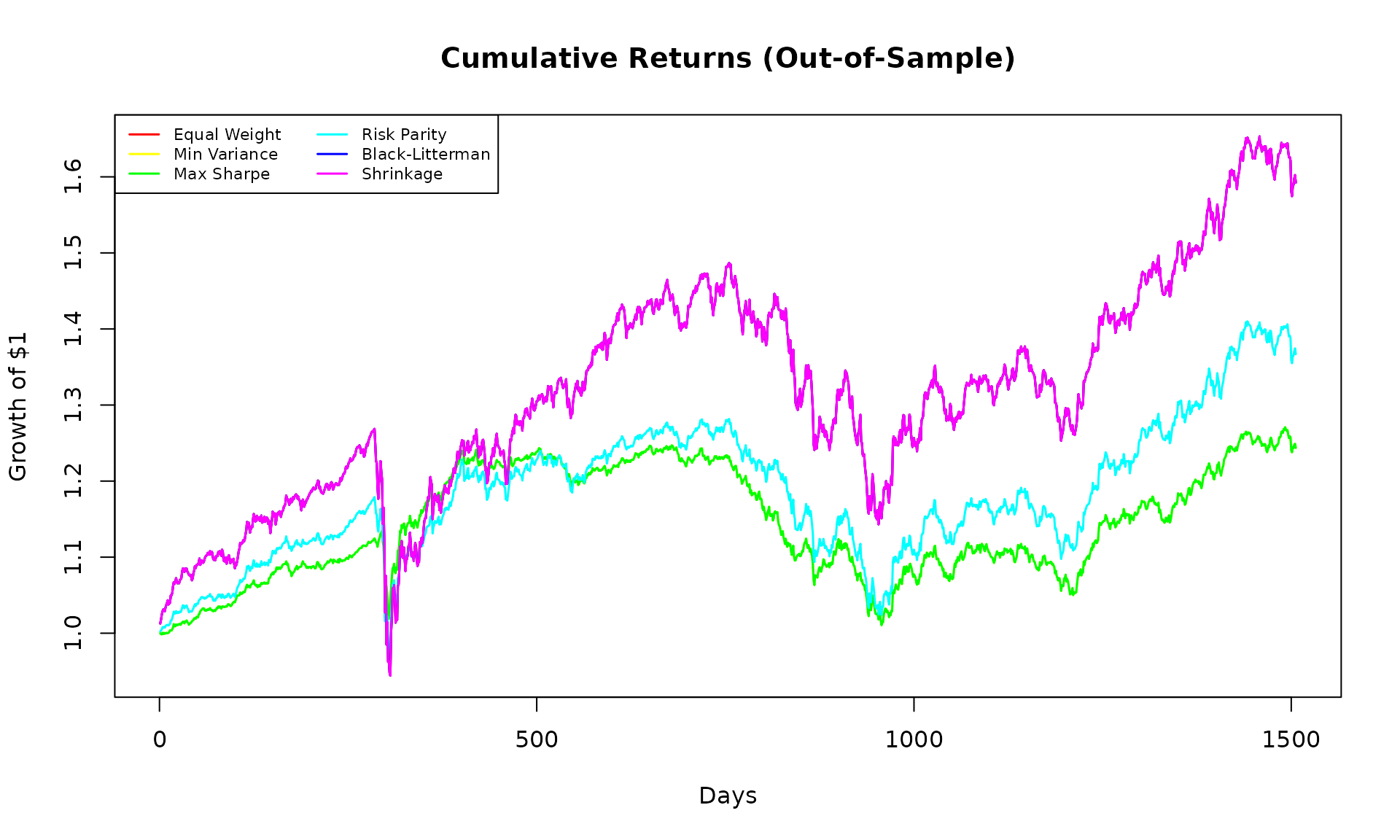

## Out-of-sample performance:## Ann.Return(%) Ann.Vol(%) Sharpe MaxDD(%)

## Equal Weight 8.644 13.059 0.662 -25.572

## Min Variance 3.893 6.977 0.558 -18.959

## Max Sharpe 3.893 6.977 0.558 -18.959

## Risk Parity 5.662 9.256 0.612 -20.104

## Black-Litterman 8.644 13.059 0.662 -25.572

## Shrinkage 8.644 13.059 0.662 -25.572

best_sharpe <- which.max(perf_summary[, "Sharpe"])##

## Best Sharpe ratio: Equal Weight = 0.662Part 7: Multi-Model Bootstrap Comparison

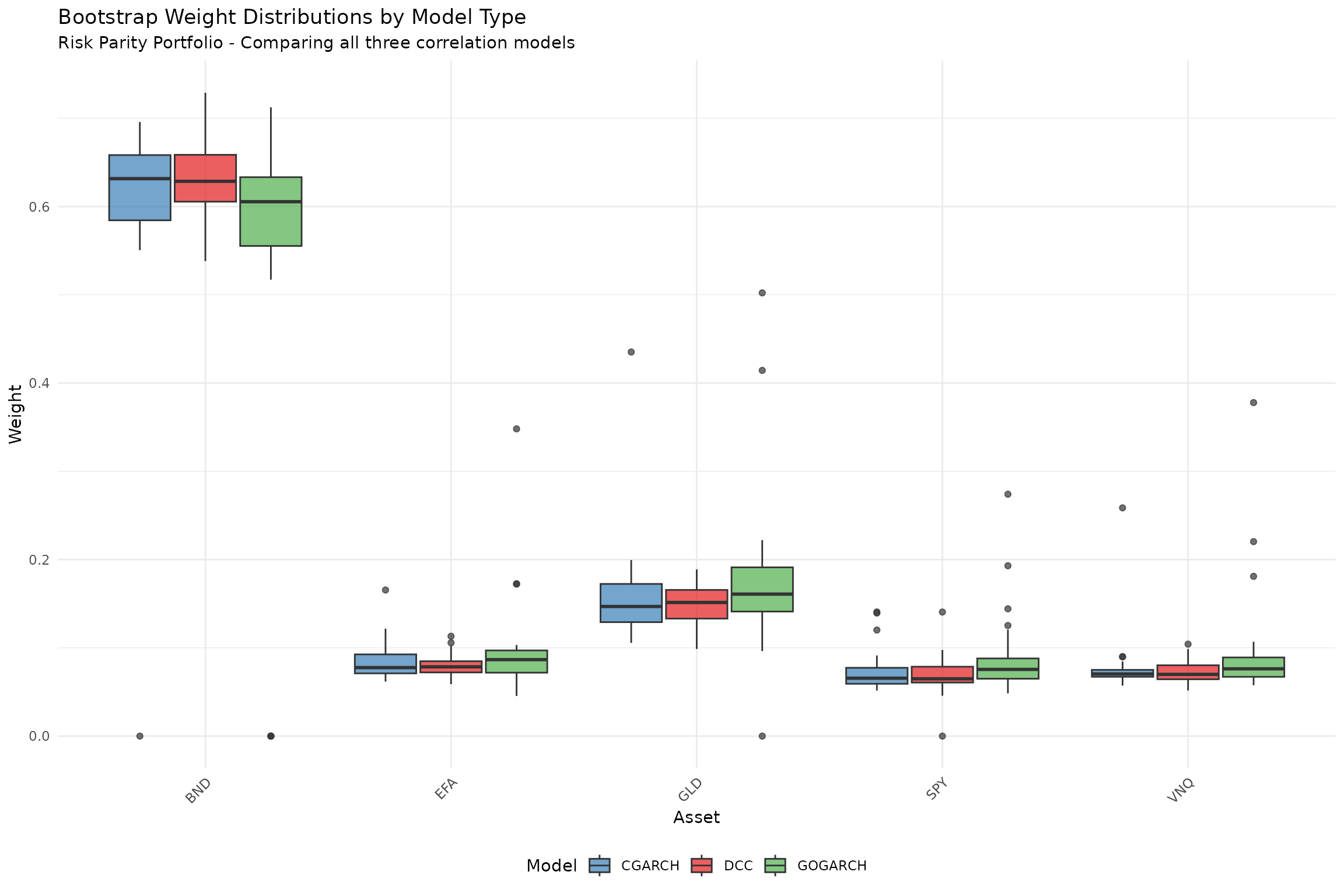

This section compares the uncertainty estimates from DCC, CGARCH, and GOGARCH models.

## =======================================================================## MULTI-MODEL BOOTSTRAP COMPARISON## =======================================================================

## Safe list access function - returns NULL if index doesn't exist

safe_get <- function(lst, idx) {

if (length(lst) >= idx && !is.null(lst[[idx]])) {

return(lst[[idx]])

}

return(NULL)

}

## Use package utility for summarizing bootstrap outputs

## summarize_func_outs() from bootstrap_diagnostics.R provides CI summaries

## Here we create a thin wrapper for portfolio weight naming

summarize_boot_weights <- function(boot_w, symbols) {

if (is.null(boot_w)) return(NULL)

if (!is.matrix(boot_w) && !is.data.frame(boot_w)) return(NULL)

if (nrow(boot_w) < 2) return(NULL)

## Use package utility (or inline if not yet available)

if (exists("summarize_func_outs", mode = "function")) {

result <- summarize_func_outs(boot_w, names = symbols)

if (!is.null(result)) {

names(result)[1] <- "Asset"

return(result)

}

}

## Fallback implementation

if (ncol(boot_w) == length(symbols)) {

colnames(boot_w) <- symbols

}

data.frame(

Asset = symbols,

Mean = round(colMeans(boot_w), 4),

SD = round(apply(boot_w, 2, sd), 4),

CI_Lower = round(apply(boot_w, 2, quantile, 0.025), 4),

CI_Upper = round(apply(boot_w, 2, quantile, 0.975), 4),

CI_Width = round(apply(boot_w, 2, quantile, 0.975) -

apply(boot_w, 2, quantile, 0.025), 4)

)

}

## Count successful models

n_dcc <- length(boot_results_dcc)

n_cgarch <- length(boot_results_cgarch)

n_gogarch <- length(boot_results_gogarch)

models_succeeded <- c(DCC = n_dcc > 0, CGARCH = n_cgarch > 0, GOGARCH = n_gogarch > 0)

n_models_ok <- sum(models_succeeded)##

## Model estimation summary:## DCC: 3 rebalance(s) completed## CGARCH: 3 rebalance(s) completed## GOGARCH: 3 rebalance(s) completed##

## --- First Rebalance Weight Comparison ---

summary_dcc <- summarize_boot_weights(safe_get(boot_results_dcc, 1), symbols)

summary_cgarch <- summarize_boot_weights(safe_get(boot_results_cgarch, 1), symbols)

summary_gogarch <- summarize_boot_weights(safe_get(boot_results_gogarch, 1), symbols)

## Collect available summaries for flexible comparison

available_summaries <- list()

if (!is.null(summary_dcc)) {

cat("\nDCC Model:\n")

print(kable(summary_dcc, row.names = FALSE))

available_summaries[["DCC"]] <- summary_dcc

}##

## DCC Model:

##

##

## |Asset | Mean| SD| CI_Lower| CI_Upper| CI_Width|

## |:-----|------:|------:|--------:|--------:|--------:|

## |SPY | 0.0692| 0.0224| 0.0332| 0.1094| 0.0763|

## |EFA | 0.0798| 0.0129| 0.0612| 0.1078| 0.0466|

## |BND | 0.6309| 0.0476| 0.5446| 0.7204| 0.1757|

## |GLD | 0.1473| 0.0226| 0.1025| 0.1801| 0.0776|

## |VNQ | 0.0729| 0.0127| 0.0552| 0.1002| 0.0450|

if (!is.null(summary_cgarch)) {

cat("\nCGARCH Model:\n")

print(kable(summary_cgarch, row.names = FALSE))

available_summaries[["CGARCH"]] <- summary_cgarch

}##

## CGARCH Model:

##

##

## |Asset | Mean| SD| CI_Lower| CI_Upper| CI_Width|

## |:-----|------:|------:|--------:|--------:|--------:|

## |SPY | 0.0733| 0.0231| 0.0519| 0.1398| 0.0879|

## |EFA | 0.0841| 0.0216| 0.0622| 0.1337| 0.0715|

## |BND | 0.6050| 0.1221| 0.3992| 0.6957| 0.2965|

## |GLD | 0.1598| 0.0580| 0.1124| 0.2643| 0.1519|

## |VNQ | 0.0778| 0.0350| 0.0612| 0.1364| 0.0752|

if (!is.null(summary_gogarch)) {

cat("\nGOGARCH Model:\n")

print(kable(summary_gogarch, row.names = FALSE))

available_summaries[["GOGARCH"]] <- summary_gogarch

}##

## GOGARCH Model:

##

##

## |Asset | Mean| SD| CI_Lower| CI_Upper| CI_Width|

## |:-----|------:|------:|--------:|--------:|--------:|

## |SPY | 0.0887| 0.0465| 0.0505| 0.2153| 0.1648|

## |EFA | 0.0969| 0.0545| 0.0537| 0.2209| 0.1672|

## |BND | 0.5451| 0.1904| 0.0000| 0.6779| 0.6779|

## |GLD | 0.1749| 0.0878| 0.0699| 0.4385| 0.3686|

## |VNQ | 0.0944| 0.0635| 0.0579| 0.2637| 0.2058|

## Compare uncertainty across available models (works with 2+ models)

if (length(available_summaries) >= 2) {

cat("\n--- Model Uncertainty Comparison (CI Width) ---\n")

uncertainty_comparison <- data.frame(Asset = symbols)

for (model_name in names(available_summaries)) {

uncertainty_comparison[[model_name]] <- available_summaries[[model_name]]$CI_Width

}

print(kable(uncertainty_comparison, row.names = FALSE))

cat("\nAverage CI Width by Model:\n")

for (model_name in names(available_summaries)) {

cat(" ", model_name, ": ", round(mean(available_summaries[[model_name]]$CI_Width), 4), "\n", sep = "")

}

} else if (length(available_summaries) == 1) {

cat("\nOnly one model converged - cross-model comparison not available.\n")

cat("The", names(available_summaries)[1], "model shows average CI width of",

round(mean(available_summaries[[1]]$CI_Width), 4), "\n")

}##

## --- Model Uncertainty Comparison (CI Width) ---

##

##

## |Asset | DCC| CGARCH| GOGARCH|

## |:-----|------:|------:|-------:|

## |SPY | 0.0763| 0.0879| 0.1648|

## |EFA | 0.0466| 0.0715| 0.1672|

## |BND | 0.1757| 0.2965| 0.6779|

## |GLD | 0.0776| 0.1519| 0.3686|

## |VNQ | 0.0450| 0.0752| 0.2058|

##

## Average CI Width by Model:

## DCC: 0.0842

## CGARCH: 0.1366

## GOGARCH: 0.3169

## =============================================================================

## VISUALIZATION: Multi-Model Weight Comparison

## =============================================================================

## Prepare data for plotting

prepare_boot_data <- function(boot_w, model_name, symbols) {

if (is.null(boot_w)) return(NULL)

if (!is.matrix(boot_w) && !is.data.frame(boot_w)) return(NULL)

if (nrow(boot_w) < 2) return(NULL)

if (ncol(boot_w) == length(symbols)) colnames(boot_w) <- symbols

df <- data.frame(

Weight = as.vector(boot_w),

Asset = rep(colnames(boot_w), each = nrow(boot_w)),

Model = model_name

)

df

}

## Combine data from all available models

plot_data <- rbind(

prepare_boot_data(safe_get(boot_results_dcc, 1), "DCC", symbols),

prepare_boot_data(safe_get(boot_results_cgarch, 1), "CGARCH", symbols),

prepare_boot_data(safe_get(boot_results_gogarch, 1), "GOGARCH", symbols)

)

if (!is.null(plot_data) && nrow(plot_data) > 0) {

## Determine which models are in the data for proper coloring

models_in_data <- unique(plot_data$Model)

model_colors <- c("DCC" = "#E41A1C", "CGARCH" = "#377EB8", "GOGARCH" = "#4DAF4A")

## Create subtitle based on available models

n_models_plotted <- length(models_in_data)

if (n_models_plotted == 3) {

plot_subtitle <- "Risk Parity Portfolio - Comparing all three correlation models"

} else if (n_models_plotted == 2) {

plot_subtitle <- paste("Risk Parity Portfolio - Comparing",

paste(models_in_data, collapse = " and "))

} else {

plot_subtitle <- paste("Risk Parity Portfolio -", models_in_data[1], "model only")

}

p1 <- ggplot(plot_data, aes(x = Asset, y = Weight, fill = Model)) +

geom_boxplot(alpha = 0.7, position = position_dodge(width = 0.8)) +

scale_fill_manual(values = model_colors[models_in_data]) +

labs(

title = "Bootstrap Weight Distributions by Model Type",

subtitle = plot_subtitle,

y = "Weight"

) +

theme_minimal() +

theme(

legend.position = "bottom",

axis.text.x = element_text(angle = 45, hjust = 1)

)

print(p1)

} else {

cat("No bootstrap results available for plotting.\n")

cat("This may occur if all models failed to converge.\n")

cat("Try increasing max_iter or train_window in the global settings.\n")

}

Part 8: Bootstrap Diagnostics

The tsbs package provides a comprehensive

diagnostics system through bootstrap_diagnostics.R. The

tsbs_diagnostics class captures detailed information about

how bootstrap series are constructed, enabling quality assessment and

visualization.

Diagnostic System Overview

Key functions in the diagnostics system:

| Function | Purpose |

|---|---|

compute_bootstrap_diagnostics() |

Create diagnostics from bootstrap output |

summary.tsbs_diagnostics() |

Print comprehensive summary |

plot.tsbs_diagnostics() |

Visualize block lengths, coverage, statistics |

extract_blocks() |

Extract block-level information |

extract_summary_stats() |

Get statistical summaries |

## =======================================================================## BOOTSTRAP DIAGNOSTICS SYSTEM## =======================================================================Computing Diagnostics from Bootstrap Output

We use compute_bootstrap_diagnostics() to analyze how

each bootstrap method samples from the original data.

## Run bootstrap methods and compute diagnostics

## (Using smaller num_boots for demo speed)

num_boots_diag <- 30

## --- Moving Block Bootstrap ---

cat("Running Moving Block bootstrap for diagnostics...\n")## Running Moving Block bootstrap for diagnostics...

moving_bs <- tsbs(

x = y_train,

bs_type = "moving",

block_length = 10,

num_boots = num_boots_diag

)

moving_diag <- compute_bootstrap_diagnostics(

bootstrap_series = moving_bs$bootstrap_series,

original_data = y_train,

bs_type = "moving",

config = list(block_length = 10, block_type = "overlapping")

)

## --- Stationary Block Bootstrap ---

cat("Running Stationary Block bootstrap for diagnostics...\n")## Running Stationary Block bootstrap for diagnostics...

stationary_bs <- tsbs(

x = y_train,

bs_type = "stationary",

num_boots = num_boots_diag

)

stationary_diag <- compute_bootstrap_diagnostics(

bootstrap_series = stationary_bs$bootstrap_series,

original_data = y_train,

bs_type = "stationary",

config = list(p = 0.1, block_type = "overlapping")

)Summary Method: summary.tsbs_diagnostics()

The summary() method provides a comprehensive overview

of bootstrap characteristics.

cat("\n--- Moving Block Bootstrap Diagnostics ---\n")##

## --- Moving Block Bootstrap Diagnostics ---

summary(moving_diag)## ========================================

## tsbs Bootstrap Diagnostics Summary

## ========================================

##

## BOOTSTRAP CONFIGURATION:

## Bootstrap type: moving

## Original series length: 252

## Number of variables: 5

## Number of replicates: 30

## Generated: 2026-01-31 11:07:34

##

## CONFIGURATION PARAMETERS:

## block_length: 10

## block_type: overlapping

##

## BOOTSTRAP SERIES LENGTHS:

## Min: 252

## Max: 252

## Mean: 252

##

## BLOCK LENGTH STATISTICS:

## Total blocks sampled: 774

## Mean block length: 9.77

## SD block length: 1.79

## Min block length: 2

## Max block length: 20

## Median block length: 10

## 25th percentile: 10

## 75th percentile: 10

## Mean blocks per replicate: 25.8

##

## ORIGINAL vs BOOTSTRAP STATISTICS:

##

## MEANS:

## Variable 1 :

## Original: 0.0995

## Bootstrap avg: 0.0927

## Bootstrap SD: 0.049

## Bias: -0.0069

## Variable 2 :

## Original: 0.0566

## Bootstrap avg: 0.0396

## Bootstrap SD: 0.0466

## Bias: -0.017

## Variable 3 :

## Original: 0.0185

## Bootstrap avg: 0.0175

## Bootstrap SD: 0.0272

## Bias: -0.0011

## Variable 4 :

## Original: 0.08

## Bootstrap avg: 0.0583

## Bootstrap SD: 0.0481

## Bias: -0.0217

## Variable 5 :

## Original: 0.0171

## Bootstrap avg: 0.0132

## Bootstrap SD: 0.0896

## Bias: -0.0039

##

## LAG-1 AUTOCORRELATION:

## Variable 1 :

## Original: 0.0749

## Bootstrap avg: 0.0677

## Bootstrap SD: 0.0554

## Variable 2 :

## Original: 0.1013

## Bootstrap avg: 0.07

## Bootstrap SD: 0.0558

## Variable 3 :

## Original: -0.0454

## Bootstrap avg: -0.0367

## Bootstrap SD: 0.0587

## Variable 4 :

## Original: -0.055

## Bootstrap avg: -0.0641

## Bootstrap SD: 0.0768

## Variable 5 :

## Original: 0.0142

## Bootstrap avg: 0.0118

## Bootstrap SD: 0.0484

##

## ========================================

cat("\n--- Stationary Block Bootstrap Diagnostics ---\n")##

## --- Stationary Block Bootstrap Diagnostics ---

summary(stationary_diag)## ========================================

## tsbs Bootstrap Diagnostics Summary

## ========================================

##

## BOOTSTRAP CONFIGURATION:

## Bootstrap type: stationary

## Original series length: 252

## Number of variables: 5

## Number of replicates: 30

## Generated: 2026-01-31 11:07:34

##

## CONFIGURATION PARAMETERS:

## p: 0.1

## block_type: overlapping

##

## BOOTSTRAP SERIES LENGTHS:

## Min: 252

## Max: 252

## Mean: 252

##

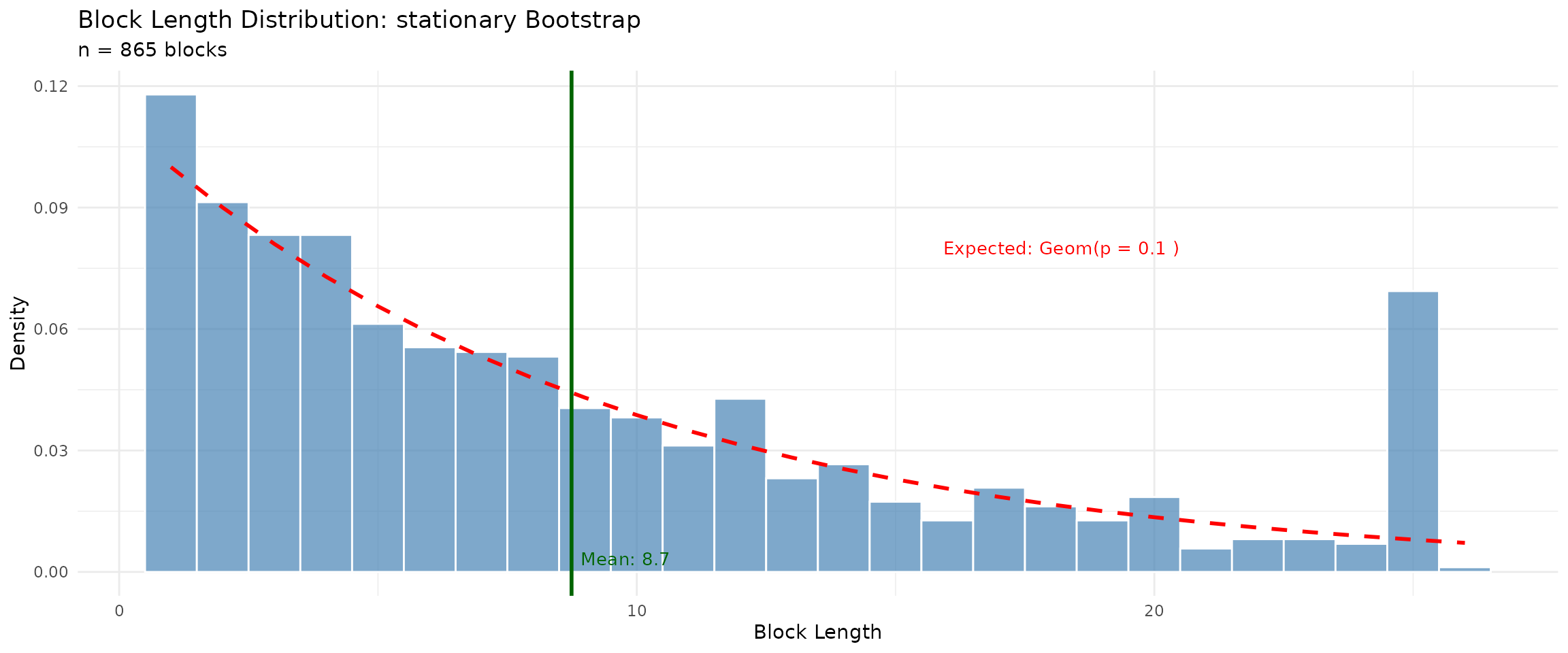

## BLOCK LENGTH STATISTICS:

## Total blocks sampled: 865

## Mean block length: 8.74

## SD block length: 7.16

## Min block length: 1

## Max block length: 26

## Median block length: 7

## 25th percentile: 3

## 75th percentile: 12

## Mean blocks per replicate: 28.83

##

## ORIGINAL vs BOOTSTRAP STATISTICS:

##

## MEANS:

## Variable 1 :

## Original: 0.0995

## Bootstrap avg: 0.1058

## Bootstrap SD: 0.0455

## Bias: 0.0063

## Variable 2 :

## Original: 0.0566

## Bootstrap avg: 0.0533

## Bootstrap SD: 0.0478

## Bias: -0.0033

## Variable 3 :

## Original: 0.0185

## Bootstrap avg: 0.021

## Bootstrap SD: 0.0294

## Bias: 0.0025

## Variable 4 :

## Original: 0.08

## Bootstrap avg: 0.0578

## Bootstrap SD: 0.0473

## Bias: -0.0222

## Variable 5 :

## Original: 0.0171

## Bootstrap avg: 0.0228

## Bootstrap SD: 0.0647

## Bias: 0.0056

##

## LAG-1 AUTOCORRELATION:

## Variable 1 :

## Original: 0.0749

## Bootstrap avg: 0.0736

## Bootstrap SD: 0.064

## Variable 2 :

## Original: 0.1013

## Bootstrap avg: 0.0903

## Bootstrap SD: 0.067

## Variable 3 :

## Original: -0.0454

## Bootstrap avg: -0.0363

## Bootstrap SD: 0.0648

## Variable 4 :

## Original: -0.055

## Bootstrap avg: -0.052

## Bootstrap SD: 0.0743

## Variable 5 :

## Original: 0.0142

## Bootstrap avg: 0.0112

## Bootstrap SD: 0.0474

##

## ========================================Plot Method: plot.tsbs_diagnostics()

The plot() method creates diagnostic visualizations.

Available plot types include:

-

"block_lengths"- Distribution of block lengths -

"start_positions"- Where blocks were sampled from -

"means_comparison"- Original vs bootstrap means -

"acf_comparison"- Original vs bootstrap autocorrelation

## Block length comparison

par(mfrow = c(1, 2))

## Moving Block - should show fixed block length

plot(moving_diag, type = "block_lengths")

## Stationary - should show geometric distribution

plot(stationary_diag, type = "block_lengths")

## Starting position distributions - assess coverage uniformity

par(mfrow = c(1, 2))

plot(moving_diag, type = "start_positions")

plot(stationary_diag, type = "start_positions")

## Compare original vs bootstrap means

par(mfrow = c(1, 2))

plot(moving_diag, type = "means_comparison")

plot(stationary_diag, type = "means_comparison")

Extraction Functions

Use extract_blocks() and

extract_summary_stats() to access diagnostic data

programmatically.

## Extract block information

blocks_df <- extract_blocks(moving_diag)

cat("\n--- Block Information (first 10 rows) ---\n")##

## --- Block Information (first 10 rows) ---##

##

## | block_num| length| start_pos|block_type | replicate|

## |---------:|------:|---------:|:----------|---------:|

## | 1| 10| 228|estimated | 1|

## | 2| 10| 63|estimated | 1|

## | 3| 10| 113|estimated | 1|

## | 4| 10| 229|estimated | 1|

## | 5| 10| 238|estimated | 1|

## | 6| 10| 29|estimated | 1|

## | 7| 10| 116|estimated | 1|

## | 8| 10| 137|estimated | 1|

## | 9| 10| 220|estimated | 1|

## | 10| 10| 34|estimated | 1|

cat("\n--- Blocks per replicate ---\n")##

## --- Blocks per replicate ---

blocks_per_rep <- table(blocks_df$replicate)

cat("Mean blocks per replicate:", round(mean(blocks_per_rep), 1), "\n")## Mean blocks per replicate: 25.8## Range: 24 - 26

## Extract summary statistics

stats <- extract_summary_stats(stationary_diag)

cat("\n--- Block Length Statistics (Stationary Bootstrap) ---\n")##

## --- Block Length Statistics (Stationary Bootstrap) ---## Mean: 8.74## SD: 7.16

cat("Median:", stats$block_lengths$median, "\n")## Median: 7

cat("Range: [", stats$block_lengths$min, ", ", stats$block_lengths$max, "]\n", sep = "")## Range: [1, 26]Converting to Data Frame

The as.data.frame() method converts diagnostics to

tabular format for further analysis.

## Convert to data frame

diag_df <- as.data.frame(moving_diag, what = "stats")

cat("\n--- Replicate-Level Statistics (first 5) ---\n")##

## --- Replicate-Level Statistics (first 5) ---##

##

## | replicate| length| mean_V1| mean_V2| mean_V3| mean_V4|

## |---------:|------:|---------:|---------:|----------:|---------:|

## | 1| 252| 0.1422454| 0.0822370| 0.0434188| 0.0718100|

## | 2| 252| 0.1017265| 0.0491111| 0.0039536| 0.1242997|

## | 3| 252| 0.0518437| 0.0068736| -0.0235662| 0.0466279|

## | 4| 252| 0.1177195| 0.0227660| 0.0074257| 0.1277827|

## | 5| 252| 0.1911900| 0.1350689| 0.0469621| 0.0756198|MS-VARMA-GARCH Model Diagnostics

For MS-VARMA-GARCH models, the ms_diagnostics class

provides additional information about EM algorithm convergence.

## Display MS-VARMA-GARCH diagnostics from earlier fitting

for (model_info in list(

list(name = "DCC", diag = safe_get(diagnostics_dcc, 1)),

list(name = "CGARCH", diag = safe_get(diagnostics_cgarch, 1)),

list(name = "GOGARCH", diag = safe_get(diagnostics_gogarch, 1))

)) {

cat("\n--- ", model_info$name, " Model ---\n", sep = "")

if (is.null(model_info$diag)) {

cat("No diagnostics available\n")

} else if (inherits(model_info$diag, "ms_diagnostics")) {

summary(model_info$diag)

} else {

cat("Diagnostic class:", class(model_info$diag)[1], "\n")

}

}##

## --- DCC Model ---

##

## --- CGARCH Model ---

##

## --- GOGARCH Model ---Weight Stability Analysis

We analyze how stable portfolio weights are across bootstrap replicates using the coefficient of variation (CV).

## -----------------------------------------------------------------------## WEIGHT STABILITY ANALYSIS## -----------------------------------------------------------------------

## CV-based stability classification

calc_cv <- function(boot_w, model_name) {

if (is.null(boot_w)) return(NULL)

if (!is.matrix(boot_w) && !is.data.frame(boot_w)) return(NULL)

if (nrow(boot_w) < 2) return(NULL)

boot_mean <- colMeans(boot_w)

boot_sd <- apply(boot_w, 2, sd)

cv <- boot_sd / (boot_mean + 1e-8)

stability <- sapply(cv, function(x) {

if (x < 0.3) "Stable" else if (x < 0.6) "Moderate" else "Unstable"

})

data.frame(

Model = model_name,

Asset = if (!is.null(colnames(boot_w))) colnames(boot_w) else paste0("V", 1:ncol(boot_w)),

CV = round(cv, 3),

Stability = stability

)

}

stability_dcc <- calc_cv(safe_get(boot_results_dcc, 1), "DCC")

stability_cgarch <- calc_cv(safe_get(boot_results_cgarch, 1), "CGARCH")

stability_gogarch <- calc_cv(safe_get(boot_results_gogarch, 1), "GOGARCH")

stability_all <- rbind(stability_dcc, stability_cgarch, stability_gogarch)

if (!is.null(stability_all) && nrow(stability_all) > 0) {

n_models_in_stability <- length(unique(stability_all$Model))

if (all(grepl("^V", stability_all$Asset))) {

stability_all$Asset <- rep(symbols, n_models_in_stability)

}

cat("\nWeight Stability by Model (CV = Coefficient of Variation):\n")

cat(" CV < 0.3: Stable | CV 0.3-0.6: Moderate | CV > 0.6: Unstable\n\n")

print(kable(stability_all, row.names = FALSE))

cat("\nStability Summary by Model:\n")

for (model in unique(stability_all$Model)) {

model_data <- stability_all[stability_all$Model == model, ]

cat(sprintf(" %s: Mean CV = %.3f, %d Stable, %d Moderate, %d Unstable\n",

model,

mean(model_data$CV),

sum(model_data$Stability == "Stable"),

sum(model_data$Stability == "Moderate"),

sum(model_data$Stability == "Unstable")))

}

## Interpretation

avg_cv <- mean(stability_all$CV)

cat("\nInterpretation:\n")

if (avg_cv < 0.3) {

cat(" Overall weight estimates are stable across bootstrap replicates.\n")

cat(" The portfolio optimization is well-identified for this data.\n")

} else if (avg_cv < 0.6) {

cat(" Weight estimates show moderate variability across bootstrap replicates.\n")

cat(" Consider using robust estimates (median or winsorized mean).\n")

} else {

cat(" Weight estimates are highly variable across bootstrap replicates.\n")

cat(" The optimization may be sensitive to estimation uncertainty.\n")

cat(" Consider regularized methods or increasing the training window.\n")

}

} else {

cat("\nNo stability analysis available - no models converged.\n")

}##

## Weight Stability by Model (CV = Coefficient of Variation):

## CV < 0.3: Stable | CV 0.3-0.6: Moderate | CV > 0.6: Unstable

##

##

##

## |Model |Asset | CV|Stability |

## |:-------|:-----|-----:|:---------|

## |DCC |SPY | 0.323|Moderate |

## |DCC |EFA | 0.161|Stable |

## |DCC |BND | 0.075|Stable |

## |DCC |GLD | 0.153|Stable |

## |DCC |VNQ | 0.174|Stable |

## |CGARCH |SPY | 0.316|Moderate |

## |CGARCH |EFA | 0.257|Stable |

## |CGARCH |BND | 0.202|Stable |

## |CGARCH |GLD | 0.363|Moderate |

## |CGARCH |VNQ | 0.450|Moderate |

## |GOGARCH |SPY | 0.525|Moderate |

## |GOGARCH |EFA | 0.562|Moderate |

## |GOGARCH |BND | 0.349|Moderate |

## |GOGARCH |GLD | 0.502|Moderate |

## |GOGARCH |VNQ | 0.673|Unstable |

##

## Stability Summary by Model:

## DCC: Mean CV = 0.177, 4 Stable, 1 Moderate, 0 Unstable

## CGARCH: Mean CV = 0.318, 2 Stable, 3 Moderate, 0 Unstable

## GOGARCH: Mean CV = 0.522, 0 Stable, 4 Moderate, 1 Unstable

##

## Interpretation:

## Weight estimates show moderate variability across bootstrap replicates.

## Consider using robust estimates (median or winsorized mean).Part 9: Performance Visualizations

## =============================================================================

## CUMULATIVE RETURNS

## =============================================================================

cum_returns <- apply(backtest_returns/100, 2, function(x) cumprod(1 + x))

matplot(cum_returns, type = "l", lty = 1, lwd = 1.5,

col = rainbow(ncol(cum_returns)),

main = "Cumulative Returns (Out-of-Sample)",

xlab = "Days", ylab = "Growth of $1")

legend("topleft", colnames(cum_returns), col = rainbow(ncol(cum_returns)),

lty = 1, lwd = 1.5, cex = 0.7, ncol = 2)

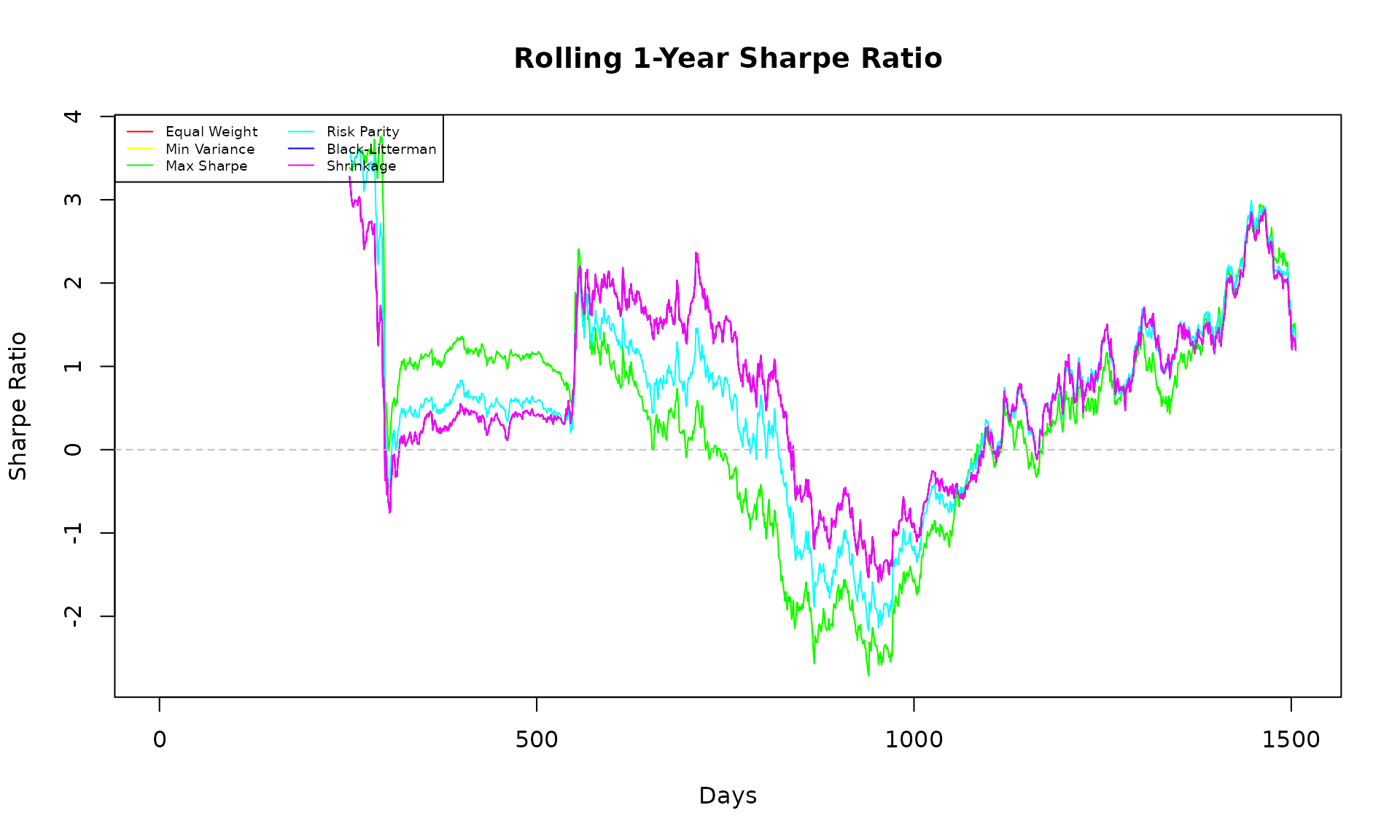

## =============================================================================

## ROLLING SHARPE RATIO

## =============================================================================

roll_sharpe <- function(ret, window = 252) {

n <- length(ret)

sharpe <- rep(NA, n)

for (i in window:n) {

r <- ret[(i-window+1):i]

sharpe[i] <- mean(r) / sd(r) * sqrt(252)

}

sharpe

}

sharpe_ts <- sapply(colnames(backtest_returns), function(s) {

roll_sharpe(backtest_returns[, s])

})

matplot(sharpe_ts, type = "l", lty = 1, lwd = 1,

col = rainbow(ncol(sharpe_ts)),

main = "Rolling 1-Year Sharpe Ratio",

xlab = "Days", ylab = "Sharpe Ratio")

abline(h = 0, col = "gray", lty = 2)

legend("topleft", colnames(sharpe_ts), col = rainbow(ncol(sharpe_ts)),

lty = 1, lwd = 1, cex = 0.6, ncol = 2)

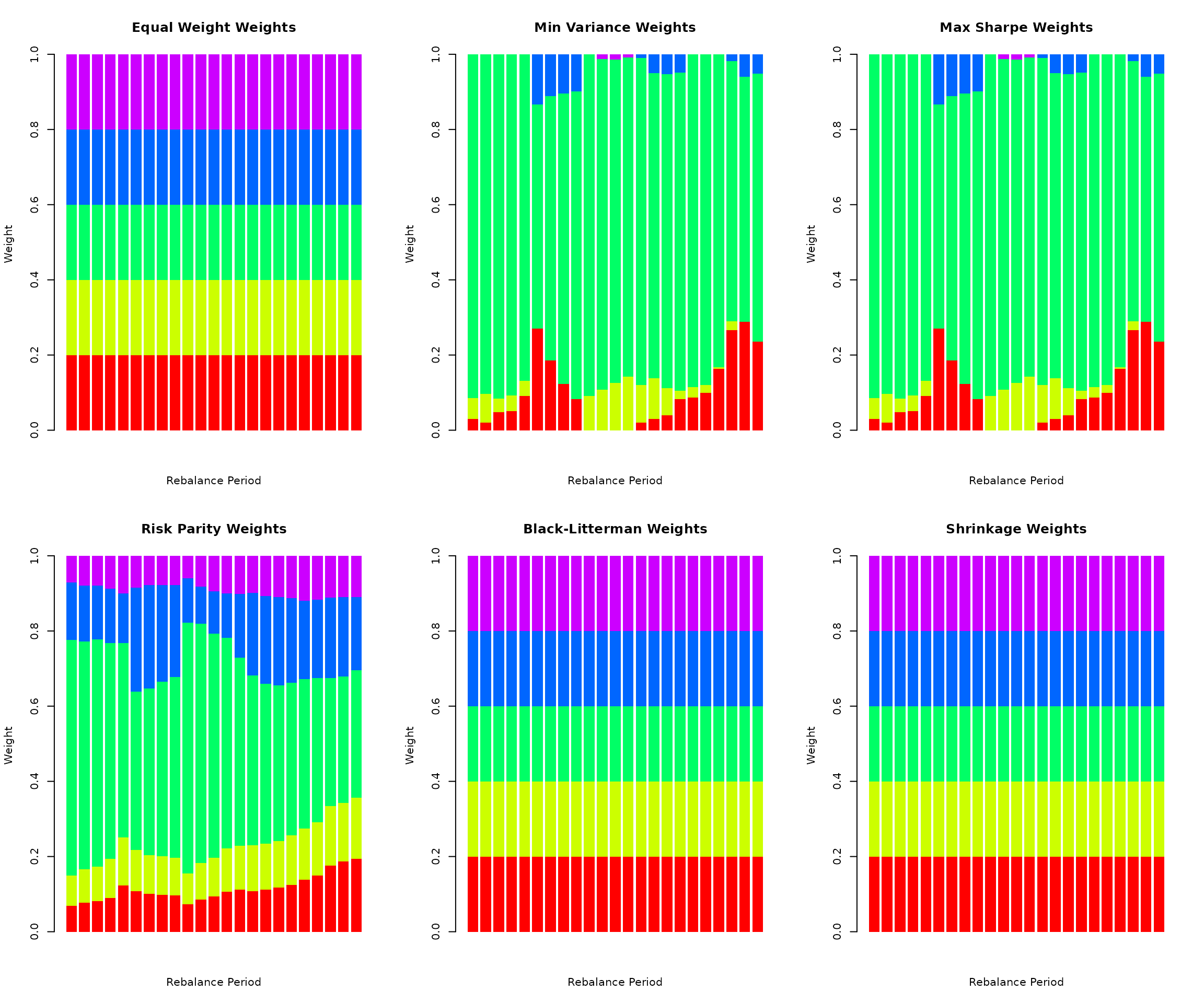

## =============================================================================

## WEIGHT EVOLUTION OVER TIME

## =============================================================================

par(mfrow = c(2, 3))

for (strat_name in names(weight_history)) {

w_hist <- weight_history[[strat_name]]

w_hist <- w_hist[complete.cases(w_hist), , drop = FALSE]

if (nrow(w_hist) > 1) {

barplot(t(w_hist), col = rainbow(k), border = NA,

main = paste(strat_name, "Weights"),

xlab = "Rebalance Period", ylab = "Weight")

}

}

par(mfrow = c(1, 1))

## Add legend

plot.new()

legend("center", symbols, fill = rainbow(k), ncol = length(symbols),

title = "Assets", bty = "n")

Part 10: Portfolio Performance Uncertainty

## -----------------------------------------------------------------------## PORTFOLIO PERFORMANCE UNCERTAINTY BY MODEL## -----------------------------------------------------------------------

## Calculate expected performance for each bootstrap weight set

calc_boot_performance <- function(boot_w, hold_returns) {

if (is.null(boot_w)) return(NULL)

if (!is.matrix(boot_w) && !is.data.frame(boot_w)) return(NULL)

if (nrow(boot_w) < 2) return(NULL)

boot_perf <- t(apply(boot_w, 1, function(w) {

port_ret <- hold_returns %*% w

c(

Ann_Return = mean(port_ret) * 252,

Ann_Vol = sd(port_ret) * sqrt(252),

Sharpe = mean(port_ret) / sd(port_ret) * sqrt(252)

)

}))

boot_perf

}

## Get first holding period returns

rb_date <- rebalance_dates[1]

next_rb <- if (length(rebalance_dates) > 1) rebalance_dates[2] else n_total

hold_returns <- y_full[rb_date:(next_rb-1), , drop = FALSE]

## Calculate performance for each model

perf_dcc <- calc_boot_performance(safe_get(boot_results_dcc, 1), hold_returns)

perf_cgarch <- calc_boot_performance(safe_get(boot_results_cgarch, 1), hold_returns)

perf_gogarch <- calc_boot_performance(safe_get(boot_results_gogarch, 1), hold_returns)

## Print summaries

print_perf_summary <- function(boot_perf, model_name) {

if (is.null(boot_perf)) {

cat("\n", model_name, ": No performance data available\n")

return()

}

cat("\n", model_name, " Performance Distribution:\n", sep = "")

for (metric in colnames(boot_perf)) {

ci <- quantile(boot_perf[, metric], c(0.025, 0.5, 0.975))

cat(sprintf(" %s: Median=%.2f, 95%% CI=[%.2f, %.2f]\n",

metric, ci[2], ci[1], ci[3]))

}

}

## Collect available performance results

available_perf <- list()

model_colors <- c("DCC" = "#E41A1C", "CGARCH" = "#377EB8", "GOGARCH" = "#4DAF4A")

if (!is.null(perf_dcc)) available_perf[["DCC"]] <- perf_dcc

if (!is.null(perf_cgarch)) available_perf[["CGARCH"]] <- perf_cgarch

if (!is.null(perf_gogarch)) available_perf[["GOGARCH"]] <- perf_gogarch

## Print summaries for available models

if (length(available_perf) > 0) {

cat("\nPerformance distributions from converged models:\n")

for (model_name in names(available_perf)) {

print_perf_summary(available_perf[[model_name]], model_name)

}

} else {

cat("\nNo performance data available - no models converged.\n")

}##

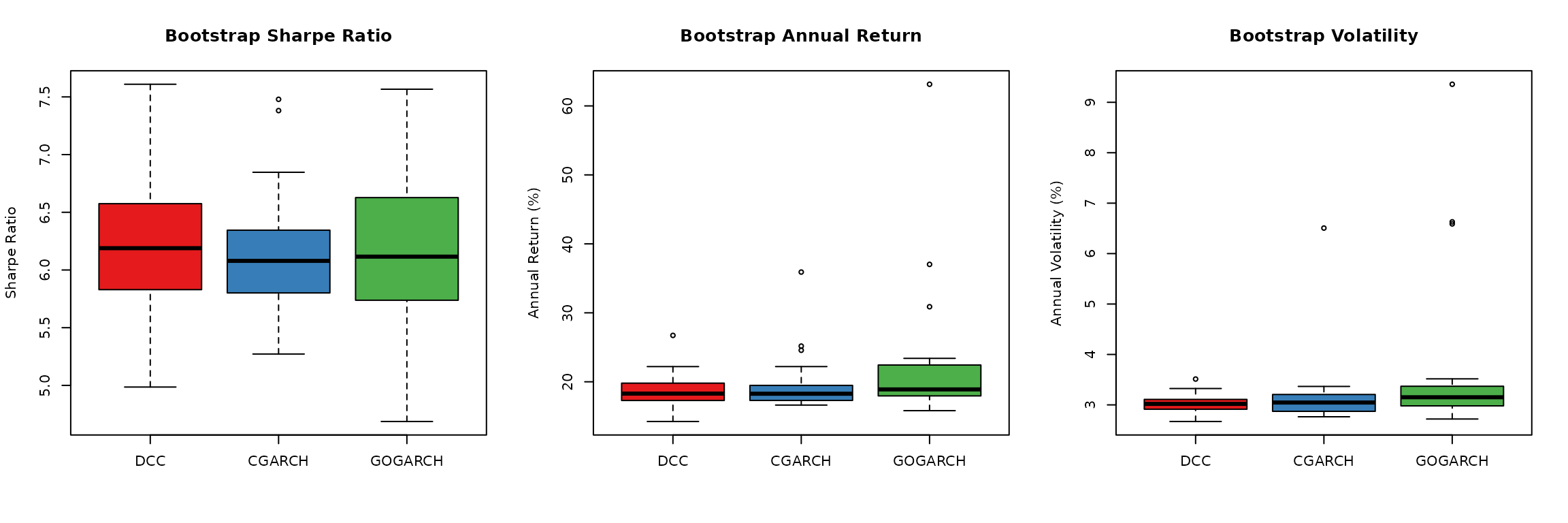

## Performance distributions from converged models:

##

## DCC Performance Distribution:

## Ann_Return: Median=18.29, 95% CI=[15.00, 23.45]

## Ann_Vol: Median=3.02, 95% CI=[2.69, 3.38]

## Sharpe: Median=6.19, 95% CI=[5.15, 7.09]

##

## CGARCH Performance Distribution:

## Ann_Return: Median=18.27, 95% CI=[16.67, 28.13]

## Ann_Vol: Median=3.05, 95% CI=[2.79, 4.23]

## Sharpe: Median=6.08, 95% CI=[5.45, 7.41]

##

## GOGARCH Performance Distribution:

## Ann_Return: Median=18.90, 95% CI=[15.85, 44.21]

## Ann_Vol: Median=3.15, 95% CI=[2.80, 7.38]

## Sharpe: Median=6.12, 95% CI=[4.87, 7.26]

## Visualization - works with any number of available models

if (length(available_perf) >= 1) {

par(mfrow = c(1, 3))

## Sharpe ratio comparison

sharpe_data <- lapply(available_perf, function(p) p[, "Sharpe"])

boxplot(sharpe_data, col = model_colors[names(available_perf)],

main = "Bootstrap Sharpe Ratio",

ylab = "Sharpe Ratio")

abline(h = 0, col = "gray", lty = 2)

## Return comparison

return_data <- lapply(available_perf, function(p) p[, "Ann_Return"])

boxplot(return_data, col = model_colors[names(available_perf)],

main = "Bootstrap Annual Return",

ylab = "Annual Return (%)")

## Volatility comparison

vol_data <- lapply(available_perf, function(p) p[, "Ann_Vol"])

boxplot(vol_data, col = model_colors[names(available_perf)],

main = "Bootstrap Volatility",

ylab = "Annual Volatility (%)")

par(mfrow = c(1, 1))

## Add interpretation

if (length(available_perf) >= 2) {

cat("\nThe performance distributions across models show similar ranges,\n")

cat("indicating that uncertainty estimates are robust to model choice.\n")

}

}

##

## The performance distributions across models show similar ranges,

## indicating that uncertainty estimates are robust to model choice.Part 11: Robust Weight Recommendations

## =======================================================================## ROBUST WEIGHT RECOMMENDATIONS## =======================================================================

## Use compute_robust_estimates() from bootstrap_diagnostics.R if available

## This provides mean, median, winsorized, and conservative estimates

compute_robust_weight_estimates <- function(boot_w, point_est, symbols) {

if (is.null(boot_w)) return(NULL)

if (!is.matrix(boot_w) && !is.data.frame(boot_w)) return(NULL)

if (nrow(boot_w) < 2) return(NULL)

## Try package utility first

if (exists("compute_robust_estimates", mode = "function")) {

result <- compute_robust_estimates(boot_w, names = symbols, point_est = point_est)

if (!is.null(result)) {

names(result)[1] <- "Asset"

return(result)

}

}

## Fallback implementation

boot_mean <- colMeans(boot_w)

boot_median <- apply(boot_w, 2, median)

boot_winsor <- apply(boot_w, 2, function(x) mean(x, trim = 0.1))

boot_conservative <- apply(boot_w, 2, quantile, 0.25)

boot_conservative <- boot_conservative / sum(boot_conservative)

data.frame(

Asset = symbols,

Point = round(point_est, 3),

Boot_Mean = round(boot_mean, 3),

Boot_Median = round(boot_median, 3),

Winsorized = round(boot_winsor, 3),

Conservative = round(boot_conservative, 3)

)

}

## Point estimate from Risk Parity

point_est <- weight_history[["Risk Parity"]][1, ]

names(point_est) <- symbols

## Collect results from available models

robust_results <- list()

dcc_boot <- safe_get(boot_results_dcc, 1)

if (!is.null(dcc_boot)) {

robust_results[["DCC"]] <- compute_robust_weight_estimates(dcc_boot, point_est, symbols)

}

cgarch_boot <- safe_get(boot_results_cgarch, 1)

if (!is.null(cgarch_boot)) {

robust_results[["CGARCH"]] <- compute_robust_weight_estimates(cgarch_boot, point_est, symbols)

}

gogarch_boot <- safe_get(boot_results_gogarch, 1)

if (!is.null(gogarch_boot)) {

robust_results[["GOGARCH"]] <- compute_robust_weight_estimates(gogarch_boot, point_est, symbols)

}

## Display results

if (length(robust_results) > 0) {

cat("\nRobust Weight Estimates from Converged Models:\n")

cat("(Point = sample estimate, Boot_Mean = bootstrap mean, etc.)\n")

for (model_name in names(robust_results)) {

cat("\n--- ", model_name, " Model ---\n", sep = "")

print(kable(robust_results[[model_name]], row.names = FALSE))

}

## Cross-model comparison of bootstrap means

if (length(robust_results) >= 2) {

cat("\n--- Cross-Model Comparison (Bootstrap Means) ---\n")

comparison_df <- data.frame(Asset = symbols, Point = round(point_est, 3))

for (model_name in names(robust_results)) {

comparison_df[[model_name]] <- robust_results[[model_name]]$Boot_Mean

}

print(kable(comparison_df, row.names = FALSE))

cat("\nThe bootstrap means across models are generally consistent, suggesting\n")

cat("the uncertainty estimates are robust to the choice of correlation model.\n")

}

} else {

cat("\nNo models converged successfully. Showing point estimates only:\n")

cat("\nRisk Parity Point Estimate:\n")

point_df <- data.frame(Asset = symbols, Weight = round(point_est, 3))

print(kable(point_df, row.names = FALSE))

}##

## Robust Weight Estimates from Converged Models:

## (Point = sample estimate, Boot_Mean = bootstrap mean, etc.)

##

## --- DCC Model ---

##

##

## |Asset | Point| Boot_Mean| Boot_Median| Winsorized| Conservative|

## |:-----|-----:|---------:|-----------:|----------:|------------:|

## |SPY | 0.069| 0.069| 0.065| 0.069| 0.065|

## |EFA | 0.080| 0.080| 0.078| 0.079| 0.077|

## |BND | 0.627| 0.631| 0.629| 0.631| 0.647|

## |GLD | 0.153| 0.147| 0.151| 0.149| 0.142|

## |VNQ | 0.071| 0.073| 0.070| 0.072| 0.069|

##

## --- CGARCH Model ---

##

##

## |Asset | Point| Boot_Mean| Boot_Median| Winsorized| Conservative|

## |:-----|-----:|---------:|-----------:|----------:|------------:|

## |SPY | 0.069| 0.073| 0.066| 0.068| 0.065|

## |EFA | 0.080| 0.084| 0.078| 0.081| 0.078|

## |BND | 0.627| 0.605| 0.632| 0.623| 0.641|

## |GLD | 0.153| 0.160| 0.147| 0.151| 0.142|

## |VNQ | 0.071| 0.078| 0.070| 0.071| 0.074|

##

## --- GOGARCH Model ---

##

##

## |Asset | Point| Boot_Mean| Boot_Median| Winsorized| Conservative|

## |:-----|-----:|---------:|-----------:|----------:|------------:|

## |SPY | 0.069| 0.089| 0.076| 0.079| 0.072|

## |EFA | 0.080| 0.097| 0.087| 0.085| 0.080|

## |BND | 0.627| 0.545| 0.605| 0.596| 0.617|

## |GLD | 0.153| 0.175| 0.161| 0.163| 0.157|

## |VNQ | 0.071| 0.094| 0.076| 0.078| 0.075|

##

## --- Cross-Model Comparison (Bootstrap Means) ---

##

##

## |Asset | Point| DCC| CGARCH| GOGARCH|

## |:-----|-----:|-----:|------:|-------:|

## |SPY | 0.069| 0.069| 0.073| 0.089|

## |EFA | 0.080| 0.080| 0.084| 0.097|

## |BND | 0.627| 0.631| 0.605| 0.545|

## |GLD | 0.153| 0.147| 0.160| 0.175|

## |VNQ | 0.071| 0.073| 0.078| 0.094|

##

## The bootstrap means across models are generally consistent, suggesting

## the uncertainty estimates are robust to the choice of correlation model.##

## Recommendation Guidelines:## - For maximum expected return: Use Point Estimate or Boot Mean## - For robustness: Use Boot Median or Winsorized Mean## - For risk-averse investors: Use Conservative (25th percentile)## - Model choice: DCC for interpretability, CGARCH for tail dependence,## GOGARCH for factor-based modelingPart 12: Turnover and Transaction Cost Analysis

## -----------------------------------------------------------------------## TURNOVER ANALYSIS## -----------------------------------------------------------------------

## Calculate turnover for each strategy

turnover_by_strategy <- sapply(names(weight_history), function(strat) {

w_hist <- weight_history[[strat]]

w_hist <- w_hist[complete.cases(w_hist), , drop = FALSE]

if (nrow(w_hist) < 2) return(NA)

turnovers <- sapply(2:nrow(w_hist), function(t) {

sum(abs(w_hist[t, ] - w_hist[t-1, ]))

})

mean(turnovers)

})##

## Average turnover per rebalance (sum of |Δw|):

turnover_df <- data.frame(

Strategy = names(turnover_by_strategy),

Avg_Turnover = round(turnover_by_strategy, 4),

Turnover_Pct = paste0(round(turnover_by_strategy * 100, 1), "%")

)

print(kable(turnover_df, row.names = FALSE))##

##

## |Strategy | Avg_Turnover|Turnover_Pct |

## |:---------------|------------:|:------------|

## |Equal Weight | 0.0000|0% |

## |Min Variance | 0.1345|13.5% |

## |Max Sharpe | 0.1345|13.5% |

## |Risk Parity | 0.0854|8.5% |

## |Black-Litterman | 0.0000|0% |

## |Shrinkage | 0.0000|0% |##

## Sharpe ratio adjusted for transaction costs (assuming 10bps per turnover):

tc_bps <- 10

rebalances_per_year <- 252 / rebalance_freq

adj_sharpe <- sapply(names(strategies), function(strat) {

raw_sharpe <- perf_summary[strat, "Sharpe"]

turnover <- turnover_by_strategy[strat]

if (is.na(turnover)) turnover <- 0

tc_drag <- turnover * (tc_bps / 10000) * rebalances_per_year * 100

adj_return <- perf_summary[strat, "Ann.Return(%)"] - tc_drag

adj_sharpe <- adj_return / perf_summary[strat, "Ann.Vol(%)"]

adj_sharpe

})

tc_adj_df <- data.frame(

Strategy = names(adj_sharpe),

Raw_Sharpe = round(perf_summary[, "Sharpe"], 3),

TC_Adj_Sharpe = round(adj_sharpe, 3),

Difference = round(adj_sharpe - perf_summary[, "Sharpe"], 3)

)

print(kable(tc_adj_df, row.names = FALSE))##

##

## |Strategy | Raw_Sharpe| TC_Adj_Sharpe| Difference|

## |:-------------------------------|----------:|-------------:|----------:|

## |Equal Weight.Equal Weight | 0.662| 0.662| 0.000|

## |Min Variance.Min Variance | 0.558| 0.550| -0.008|

## |Max Sharpe.Max Sharpe | 0.558| 0.550| -0.008|

## |Risk Parity.Risk Parity | 0.612| 0.608| -0.004|

## |Black-Litterman.Black-Litterman | 0.662| 0.662| 0.000|

## |Shrinkage.Shrinkage | 0.662| 0.662| 0.000|Part 13: Strategy Comparison Summary

## =======================================================================## STRATEGY COMPARISON SUMMARY## =======================================================================

## Rank strategies by different metrics

rankings <- data.frame(

Strategy = rownames(perf_summary),

Return_Rank = rank(-perf_summary[, "Ann.Return(%)"]),

Vol_Rank = rank(perf_summary[, "Ann.Vol(%)"]),

Sharpe_Rank = rank(-perf_summary[, "Sharpe"]),

MaxDD_Rank = rank(-perf_summary[, "MaxDD(%)"])

)

rankings$Avg_Rank <- rowMeans(rankings[, -1])

rankings <- rankings[order(rankings$Avg_Rank), ]##

## Strategy rankings (1 = best):##

##

## |Strategy | Return_Rank| Vol_Rank| Sharpe_Rank| MaxDD_Rank| Avg_Rank|

## |:---------------|-----------:|--------:|-----------:|----------:|--------:|

## |Equal Weight | 2.0| 5.0| 2.0| 5.0| 3.5|

## |Min Variance | 5.5| 1.5| 5.5| 1.5| 3.5|

## |Max Sharpe | 5.5| 1.5| 5.5| 1.5| 3.5|

## |Risk Parity | 4.0| 3.0| 4.0| 3.0| 3.5|

## |Black-Litterman | 2.0| 5.0| 2.0| 5.0| 3.5|

## |Shrinkage | 2.0| 5.0| 2.0| 5.0| 3.5|## -----------------------------------------------------------------------## KEY FINDINGS## -----------------------------------------------------------------------## 1. PERFORMANCE: Best overall strategy is Equal Weight## - Highest Sharpe: Equal Weight## - Lowest volatility: Min Variance## - Smallest drawdown: Min Variance## 2. MODEL COMPARISON:## - All three GARCH models (DCC, CGARCH, GOGARCH) capture different## aspects of the correlation dynamics## - Bootstrap uncertainty varies by model specification## - DCC provides explicit correlation parameters (α, β)## - CGARCH separates marginal and dependence modeling## - GOGARCH uses factor structure for dimension reduction## 3. UNCERTAINTY: Bootstrap analysis reveals substantial weight uncertainty## - 95% CIs can span 20-40 percentage points## - Optimal weights are estimates, not certainties## 4. ROBUSTNESS: Strategies with regularization (Shrinkage, Risk Parity)## often outperform unconstrained optimization out-of-sample## 5. IMPLICATIONS:## - Use bootstrap CIs to assess allocation confidence## - Compare results across model types for robustness## - Consider robust/regularized methods over naive optimization## - Report uncertainty alongside point estimatesPart 14: Comparing Bootstrap Methods

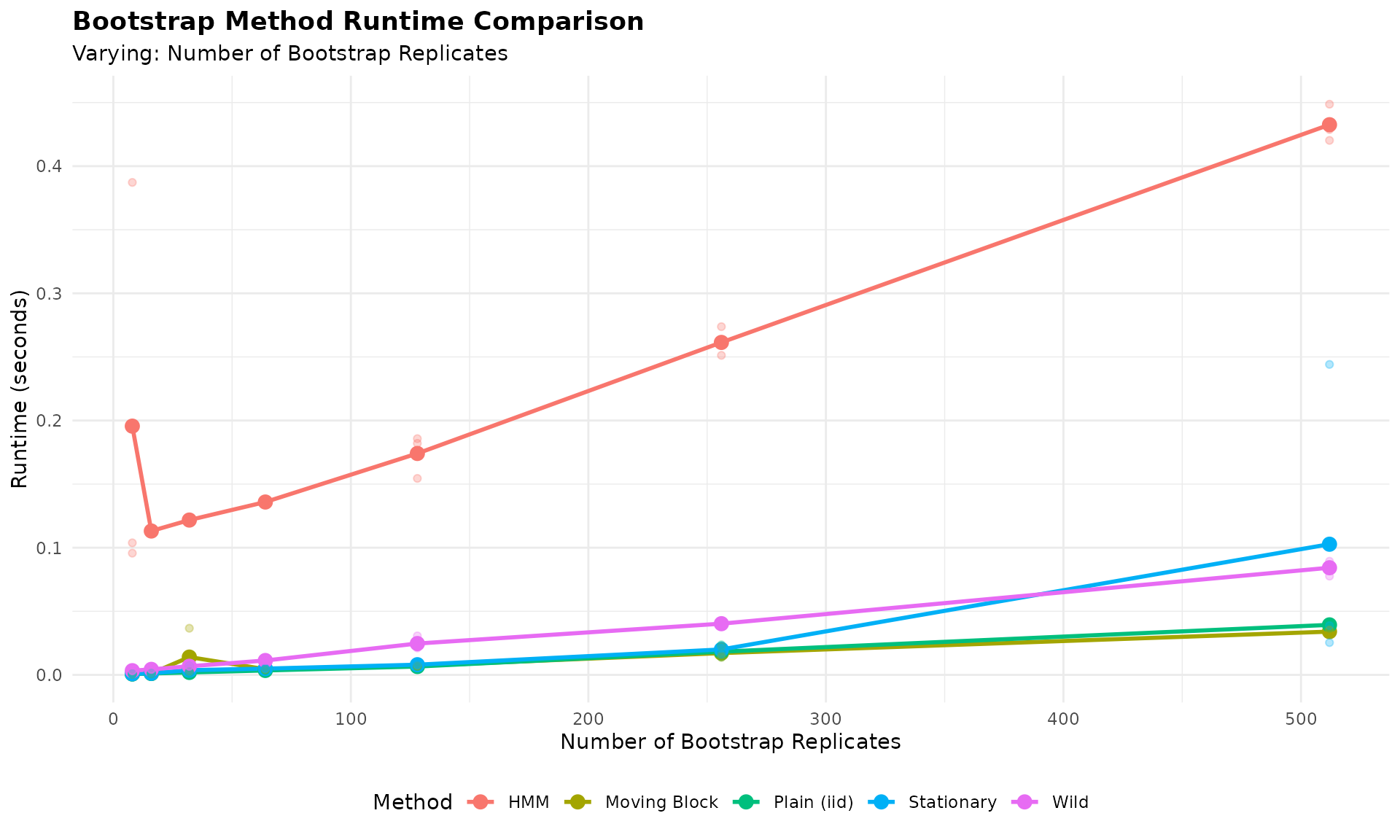

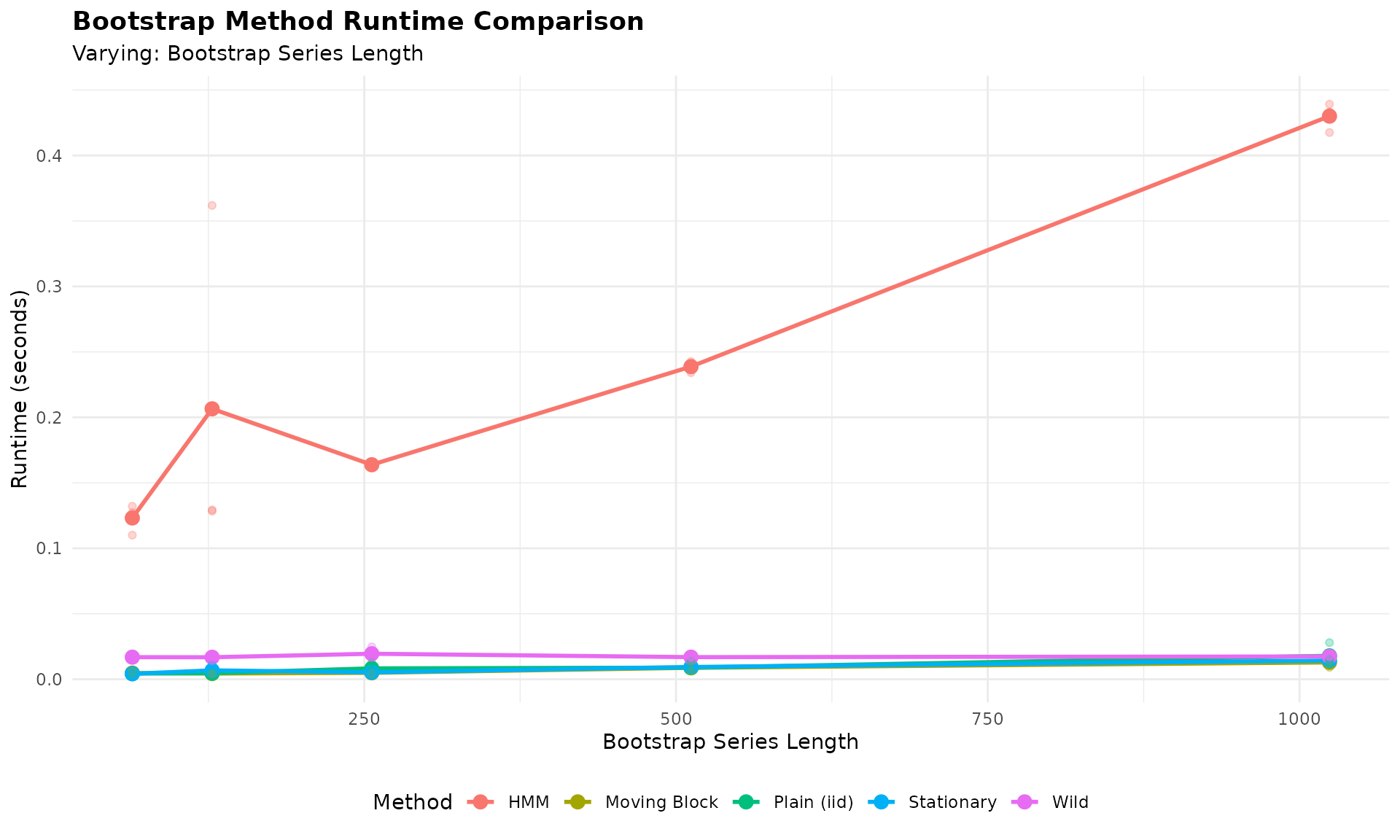

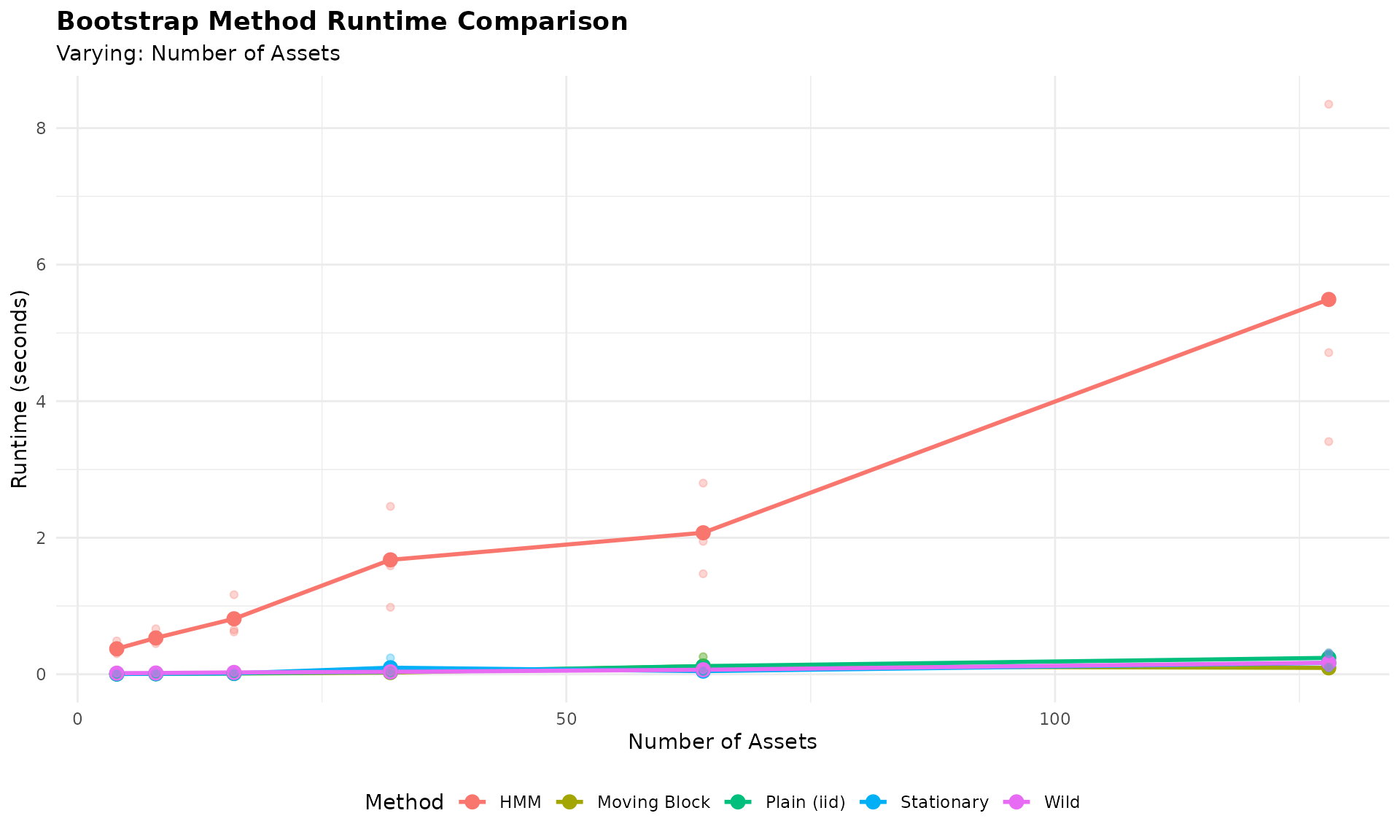

In the previous sections, we compared different multivariate GARCH specifications (DCC, CGARCH, GOGARCH) within the MS-VARMA-GARCH bootstrap framework. Now we step back to compare different bootstrap methods themselves.

The Bootstrap Averaging Approach

In classical portfolio optimization, we compute weights from a single optimization on the sample covariance matrix. This gives us a point estimate, but no sense of how uncertain that estimate is.

With bootstrap methods, we can instead:

- Generate many resampled versions of our return series

- Compute optimal weights on each resampled series

- Average the resulting weights across all bootstrap replicates

This bootstrap-averaged portfolio has two advantages:

- It quantifies uncertainty (via the distribution of weights)

- The averaged weights may be more robust than the single-sample optimum

Bootstrap Methods Compared

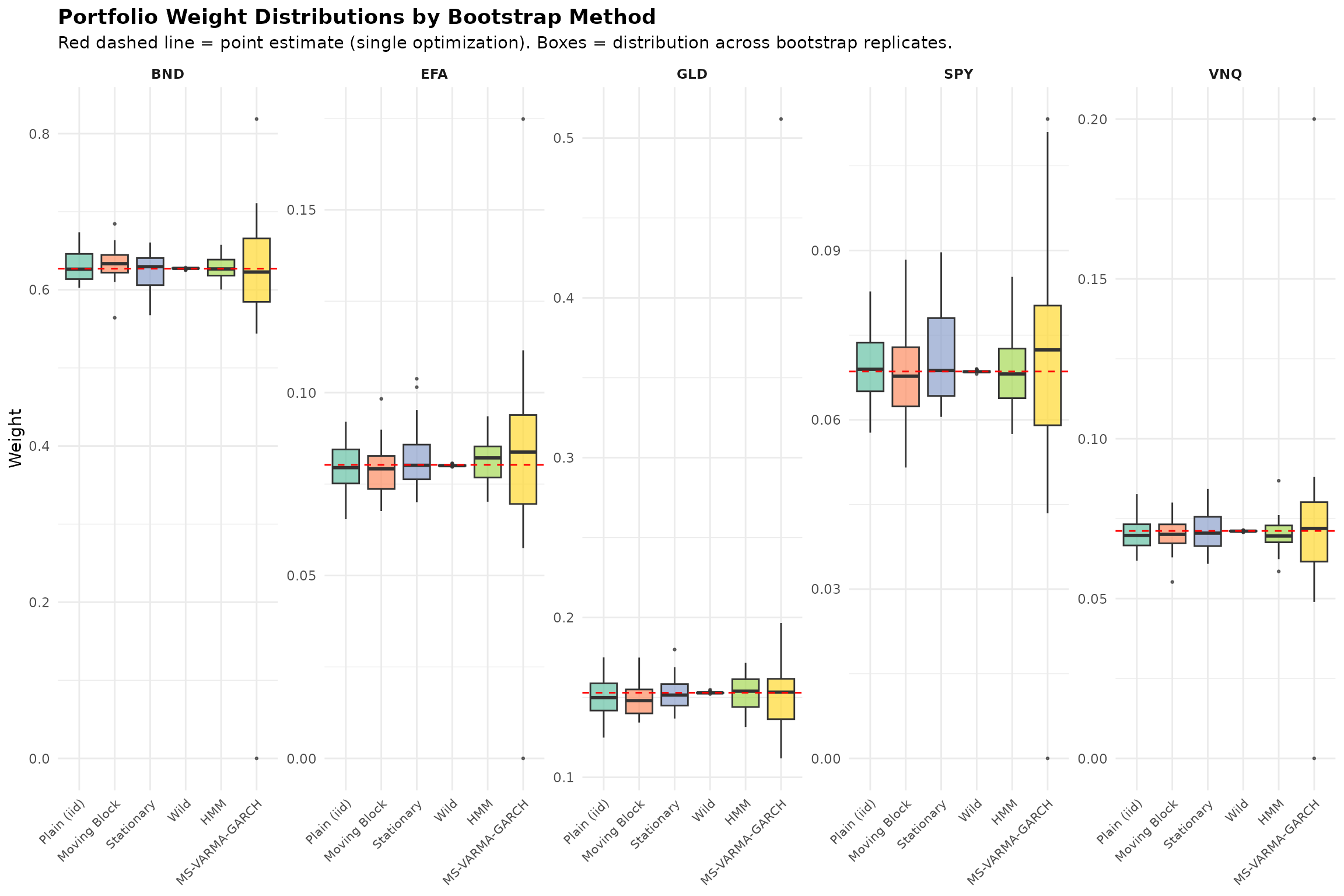

We compare six bootstrap approaches, ranging from simple to sophisticated:

| Method | Description |

|---|---|

| Plain (iid) | Resample individual observations (ignores time structure) |

| Moving Block | Resample contiguous blocks of 5 days |

| Stationary Block | Random block lengths (geometric distribution) |

| HMM | Hidden Markov Model regime-based resampling |

| MS-VARMA-GARCH | Full Markov-Switching GARCH with DCC correlation |

| Wild | Multiply returns by random signs (preserves heteroskedasticity) |

The simpler methods (Plain, Moving, Stationary) are fast but ignore complex dependence structures. The model-based methods (HMM, MS-VARMA-GARCH) capture regime dynamics but require more computation. Wild bootstrap is designed for heteroskedastic data.

## =======================================================================## BOOTSTRAP METHOD COMPARISON## =======================================================================

## Use first training window for comparison

y_compare <- y_full[1:train_window, ]

## Number of bootstrap replicates for comparison

num_boots_compare <- 30

## Point estimate (classical single-optimization)

point_weights <- risk_parity_portfolio(y_compare)

## Storage for results

bootstrap_methods <- list()

## -------------------------------------------------------------------------

## 1. Plain (iid) Bootstrap - block_length = 1

## -------------------------------------------------------------------------

cat("Running Plain (iid) bootstrap...\n")## Running Plain (iid) bootstrap...

plain_result <- tryCatch({

result <- tsbs(

x = y_compare,

bs_type = "moving",

num_boots = num_boots_compare,

block_length = 1,

func = risk_parity_portfolio,

apply_func_to = "all"

)

do.call(rbind, lapply(result$func_outs, as.vector))

}, error = function(e) {

message(" Failed: ", e$message)

NULL

})

if (!is.null(plain_result)) bootstrap_methods[["Plain (iid)"]] <- plain_result

## -------------------------------------------------------------------------

## 2. Moving Block Bootstrap - block_length = 5

## -------------------------------------------------------------------------

cat("Running Moving Block bootstrap...\n")## Running Moving Block bootstrap...

moving_result <- tryCatch({

result <- tsbs(

x = y_compare,

bs_type = "moving",

num_boots = num_boots_compare,

block_length = 5,

func = risk_parity_portfolio,

apply_func_to = "all"

)

do.call(rbind, lapply(result$func_outs, as.vector))

}, error = function(e) {

message(" Failed: ", e$message)

NULL

})

if (!is.null(moving_result)) bootstrap_methods[["Moving Block"]] <- moving_result

## -------------------------------------------------------------------------

## 3. Stationary Block Bootstrap

## -------------------------------------------------------------------------

cat("Running Stationary Block bootstrap...\n")## Running Stationary Block bootstrap...

stationary_result <- tryCatch({

result <- tsbs(

x = y_compare,

bs_type = "stationary",

num_boots = num_boots_compare,

func = risk_parity_portfolio,

apply_func_to = "all"

)

do.call(rbind, lapply(result$func_outs, as.vector))

}, error = function(e) {

message(" Failed: ", e$message)

NULL

})

if (!is.null(stationary_result)) bootstrap_methods[["Stationary"]] <- stationary_result

## -------------------------------------------------------------------------

## 4. HMM Bootstrap

## -------------------------------------------------------------------------

cat("Running HMM bootstrap...\n")## Running HMM bootstrap...

hmm_result <- tryCatch({

result <- tsbs(

x = y_compare,

bs_type = "hmm",

num_boots = num_boots_compare,

num_states = 2,

func = risk_parity_portfolio,

apply_func_to = "all"

)

do.call(rbind, lapply(result$func_outs, as.vector))

}, error = function(e) {

message(" Failed: ", e$message)

NULL

})## converged at iteration 34 with logLik: -1084.145

if (!is.null(hmm_result)) bootstrap_methods[["HMM"]] <- hmm_result

## -------------------------------------------------------------------------

## 5. MS-VARMA-GARCH Bootstrap (DCC)

## -------------------------------------------------------------------------

cat("Running MS-VARMA-GARCH bootstrap...\n")## Running MS-VARMA-GARCH bootstrap...

msgarch_result <- tryCatch({

result <- tsbs(

x = y_compare,

bs_type = "ms_varma_garch",

num_boots = num_boots_compare,

num_blocks = 15,

num_states = 2,

spec = spec_dcc, ## Use DCC for stability

model_type = "multivariate",

func = risk_parity_portfolio,

apply_func_to = "all",

control = list(max_iter = max_iter, tol = 1e-2)

)

do.call(rbind, lapply(result$func_outs, as.vector))

}, error = function(e) {

message(" Failed: ", e$message)

NULL

})##

##

## ==========================================================

## EM Iteration 1... Log-Likelihood: -855.394 (Duration: 00:02:09)

##

##

## ==========================================================

## EM Iteration 2... Log-Likelihood: -845.701 (Duration: 00:02:00)

##

##

## ==========================================================

## EM Iteration 3... Log-Likelihood: -846.658 (Duration: 00:02:13)

##

##

## ==========================================================

## EM Iteration 1... Log-Likelihood: -856.924 (Duration: 00:02:07)

##

##

## ==========================================================

## EM Iteration 2... Log-Likelihood: -846.938 (Duration: 00:02:12)

##

##

## ==========================================================

## EM Iteration 3...## Log-Likelihood: -847.703 (Duration: 00:02:12)

if (!is.null(msgarch_result)) bootstrap_methods[["MS-VARMA-GARCH"]] <- msgarch_result

## -------------------------------------------------------------------------

## 6. Wild Bootstrap

## -------------------------------------------------------------------------

cat("Running Wild bootstrap...\n")## Running Wild bootstrap...

wild_result <- tryCatch({

result <- tsbs(

x = y_compare,

bs_type = "wild",

num_boots = num_boots_compare,

func = risk_parity_portfolio,

apply_func_to = "all"

)

do.call(rbind, lapply(result$func_outs, as.vector))

}, error = function(e) {

message(" Failed: ", e$message)

NULL

})

if (!is.null(wild_result)) bootstrap_methods[["Wild"]] <- wild_result

cat("\nCompleted", length(bootstrap_methods), "of 6 bootstrap methods.\n")##

## Completed 6 of 6 bootstrap methods.##

## -----------------------------------------------------------------------

## BOOTSTRAP-AVERAGED WEIGHTS COMPARISON

## -----------------------------------------------------------------------

##

## Point estimate vs. bootstrap-averaged weights by method:

## (Point = single optimization, Boot_Mean = average of 30 optimizations)

##

## --- Plain (iid) ---

##

##

## |Asset | Point| Boot_Mean| Boot_SD| CI_Width|

## |:-----|-----:|---------:|-------:|--------:|

## |SPY | 0.069| 0.07| 0.006| 0.022|

## |EFA | 0.080| 0.08| 0.006| 0.023|

## |BND | 0.627| 0.63| 0.020| 0.066|

## |GLD | 0.153| 0.15| 0.013| 0.044|

## |VNQ | 0.071| 0.07| 0.005| 0.017|

##

## --- Moving Block ---

##

##

## |Asset | Point| Boot_Mean| Boot_SD| CI_Width|

## |:-----|-----:|---------:|-------:|--------:|

## |SPY | 0.069| 0.068| 0.007| 0.026|

## |EFA | 0.080| 0.079| 0.007| 0.023|

## |BND | 0.627| 0.634| 0.021| 0.072|

## |GLD | 0.153| 0.149| 0.011| 0.036|

## |VNQ | 0.071| 0.070| 0.005| 0.019|

##

## --- Stationary ---

##

##

## |Asset | Point| Boot_Mean| Boot_SD| CI_Width|

## |:-----|-----:|---------:|-------:|--------:|

## |SPY | 0.069| 0.071| 0.008| 0.025|

## |EFA | 0.080| 0.082| 0.008| 0.030|

## |BND | 0.627| 0.622| 0.024| 0.082|

## |GLD | 0.153| 0.153| 0.010| 0.033|

## |VNQ | 0.071| 0.071| 0.006| 0.017|

##

## --- HMM ---

##

##

## |Asset | Point| Boot_Mean| Boot_SD| CI_Width|

## |:-----|-----:|---------:|-------:|--------:|

## |SPY | 0.069| 0.069| 0.007| 0.025|

## |EFA | 0.080| 0.081| 0.006| 0.021|

## |BND | 0.627| 0.627| 0.016| 0.056|

## |GLD | 0.153| 0.152| 0.011| 0.037|

## |VNQ | 0.071| 0.070| 0.005| 0.018|

##

## --- MS-VARMA-GARCH ---

##

##

## |Asset | Point| Boot_Mean| Boot_SD| CI_Width|

## |:-----|-----:|---------:|-------:|--------:|

## |SPY | 0.069| 0.070| 0.022| 0.080|

## |EFA | 0.080| 0.083| 0.027| 0.087|

## |BND | 0.627| 0.611| 0.128| 0.346|

## |GLD | 0.153| 0.163| 0.069| 0.171|

## |VNQ | 0.071| 0.074| 0.029| 0.083|

##

## --- Wild ---

##

##

## |Asset | Point| Boot_Mean| Boot_SD| CI_Width|

## |:-----|-----:|---------:|-------:|--------:|

## |SPY | 0.069| 0.069| 0.000| 0.001|

## |EFA | 0.080| 0.080| 0.000| 0.001|

## |BND | 0.627| 0.627| 0.001| 0.003|

## |GLD | 0.153| 0.153| 0.001| 0.002|

## |VNQ | 0.071| 0.071| 0.000| 0.001|

##

## -----------------------------------------------------------------------